E&S Tools and Resources

Environmental & Social Management (ESMS) System Diagnostic Tool for Financial Institutions (FIs)

The ESMS Diagnostic Tool for FIs is designed to enable IFC, FIs, institutional investors, and asset managers to assess or self-assess the quality of an ESMS and benchmark it against IFC's Performance Standard 1 and good market practices. The ESMS Diagnostic Tool assesses nine key elements of a financial institution's ESMS System and classifies them on the basis of their level of advancement.

Risk Categorization Table

Factors such as scale, location, sensitivity and magnitude of impacts of a project need to be considered on a case by case basis. For example, some hotel/tourism developments may be categorized as A, rather than B.

The examples of project categorization provided below are for illustrative purposes only.

Training

The IFC and other Development Finance Institutions offer training platforms on E&S risk management and environmental business opportunities.

IFC’s Sustainability Training & E-Learning Program (STEP):Designed for managers and staff of financial institutions (FIs), this e-training, available in English, French and Russian, represents the next generation of products designed to help financial institutions better understand sustainable finance, environmental and social risk management and explore sustainability-related business opportunities.

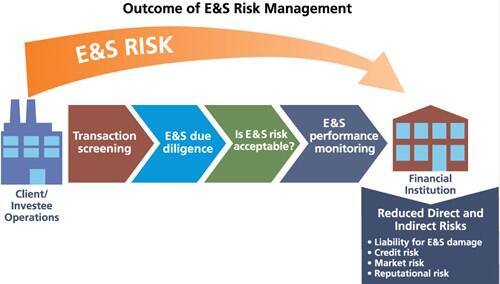

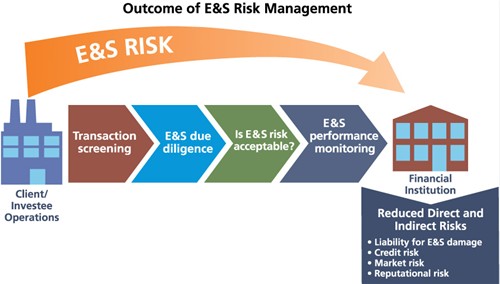

What is an ESMS?

A Environmental and Social Management System is a set of policies, procedures, tools and internal capacity to identify and manage a financial institution's exposure to the environmental and social risks of its clients/investees.

A Environmental and Social Management System states a financial institution’s commitment to environmental and social management, explains its procedures for identifying, assessing and managing environmental and social risk of financial transactions, defines the decision-making process, describes the roles, responsibilities and capacity needs of staff for doing so and states the documentation and recordkeeping requirements. It also provides guidance on how to screen transactions, categorize transactions based on their environmental and social risk, conduct environmental and social due diligence and monitor the client’s/investee’s environmental and social performance.

The scope of financing activities of different types of financial institutions varies greatly, and so do the associated environmental and social risks. The management of these risks should also be tailored to the individual institutional characteristics of each financial institution, which are different for banking institutions, leasing companies, microfinance institutions, and private equity funds.

The supporting policies and procedures of the ESMS should be well documented, made available to all staff with responsibilities for implementation and can be compiled into a stand-alone operations manual to formally document the process. This manual should be updated regularly through a simple but effective revision process.

Because the procedures and decision-making process of the ESMS are systematically incorporated at each stage of transaction appraisal and monitoring, the ESMS cannot function as a stand-alone system. The process for developing a ESMS needs to consider a financial institution’s existing risk management framework and transaction cycle.

ESMS for Banking Institution

A banking institution's exposure to environmental and social risks varies greatly as a function of the clients within its portfolio and the types of financial transactions, which should be reflected in the scope of the ESMS.

The scope of financing activities of banking institutions may encompass transactions that target corporate finance, housing, project finance, retail, short-term finance, and small-medium enterprises.

ESMS for Leasing Company

The scope of financing activities of leasing companies encompasses transactions that vary in duration and consist of finance leases or operating leases of assets such as office equipment, vehicles, properties, and specialized equipment and machinery.

ESMS for Microfinance Institution

The scope of financing activities of microfinance institutions encompasses transactions that are of smaller amounts than those of banking institutions, focusing on commercial clients whose operations are generally small.

ESMS for Private Equity Fund

The scope of financing activities of private equity funds encompasses transactions that are direct equity investments in companies, generally for a fixed term, which are later sold in excess of the price initially paid for the investment.

Due to the legal nature of the transaction, which makes the private equity fund a partial or full owner of an investee company, the private equity fund is directly exposed to, and thus also liable for, the environmental and social risks of the investee company.

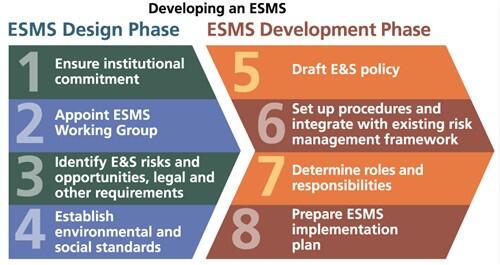

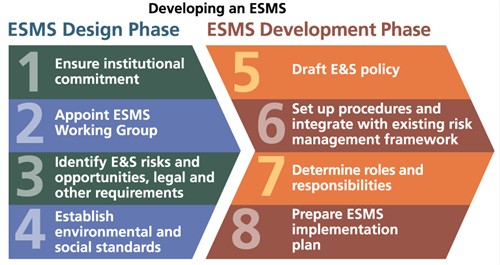

Developing an ESMS

Developing a ESMS requires senior management support and needs to be integrated with the financial institution's existing risk management framework.

Developing a ESMS is most effective and efficient if it is supported by senior management and integrated with the financial institution’s existing risk management framework. A financial institution can initiate the process for developing a ESMS by establishing a Working Group.

An ESMS includes a policy, a set of procedures to identify, assess and manage environmental and social risks in financial transactions and internal capacity of staff responsible for environmental and social management and investments.

It should be designed to manage the level of environmental and social risk that the financial institution is exposed to through its portfolio, both in terms of the industry sector of its clients/investees and the type of financial transactions. The management of these risks should be tailored to the organizational needs of each financial institution, which are different for banking institutions, leasing companies, microfinance institutions, and private equity funds.

Tips from Lessons Learned

Here are ten lessons for effective integration of sustainability into the policies, practices, products, and services of financial institutions.

Based on the experiences of financial institutions taking concrete steps to integrate sustainability into their policies, practices, products, and services, IFC’s report on Banking on Sustainability reveals the following 10 lessons for effective integration:

Initiate ESMS Development Process

A financial institution's internal process for developing a ESMS may vary based on its organizational characteristics. The process can be initiated by establishing an ESMS Working Group, which is responsible for developing the ESMS.

Tasks of ESMS Working Group

The ESMS Working Group should review the financial institution's exposure to environmental and social risk through its portfolio and develop the necessary procedures for evaluating and managing environmental and social risk.

To start the process of developing a ESMS, the ESMS Working Group should analyze the financial institution’s portfolio to gain an understanding of the financial institution’s exposure to environmental and social risk, including the industry sectors of clients/investees and transaction type.

Institutional Commitment

An ESMS can only function effectively and properly if its development and implementation is supported by the financial institution itself.

As with any other internal management system, an ESMS can only function effectively and properly if its development and implementation is supported by the financial institution itself. This requires ownership, dedication and commitment by the financial institution to allocate the necessary resources for the successful development of an ESMS.

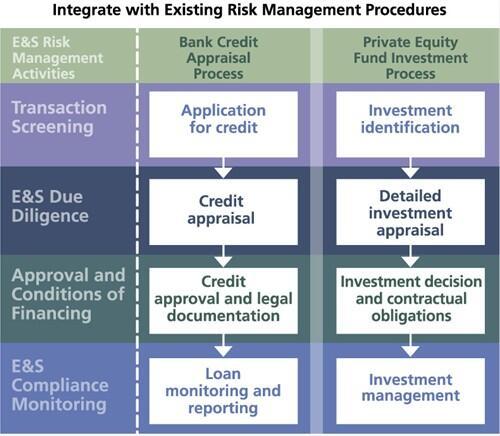

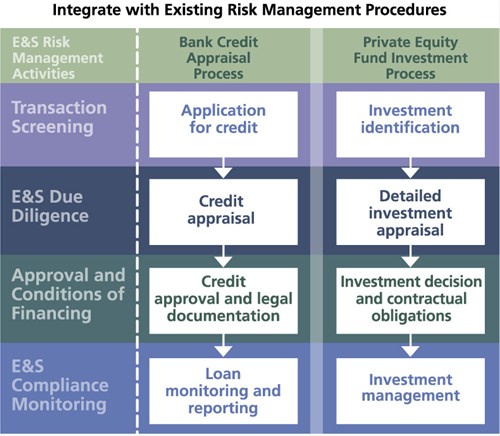

Integrate with Existing Risk Procedures

To be effective and cost-efficient, a financial institution's ESMS needs to be fully integrated into its existing risk management framework and it will be necessary to revise the existing procedures.

The procedures for managing environmental and social risk need to be applied in tandem with other risk management procedures already in place at each stage of the transaction cycle. To ensure this, a financial institution may need to revise the procedures that support its existing risk management framework by incorporating considerations for environmental and social risk throughout the transaction cycle or developing a stand-alone ESMS operations manual to formally document the environmental and social risk management process.

The financial institution’s documentation associated with each stage of the transaction cycle should be revised to incorporate environmental and social risk considerations or new forms should be developed, if necessary. A financial institution’s transaction cycle typically includes:

- Identification. The Loan Officers/Relationship Managers at a financial institution identify a potential transaction or are approached by a potential client/investee. The scope of potential transactions that a financial institution will consider will be based on its own financing objectives, and may include a focus on certain transaction types, industry sectors, or environmental business opportunities.

- Screening. At an initial stage, the Loan Officers/Relationship Managers will determine if a proposed transaction complies with the financial institution’s requirements for financing, such as client/investee reputation and integrity. A financial institution’s requirements may also include a list of activities and industry sectors that it will not finance.

- Appraisal. The Credit Analysts/Investment Analysts will appraise the financial viability and credit risk of a proposed transaction, which generally entails a site visit. The appraisal process should also incorporate an evaluation of potential environmental and social risk associated with the transaction, based on product type and industry sector. The Credit Analysts/Investment Analysts can assign a environmental and social risk category, which will determine the level of environmental and social due diligence that will need to be conducted.

- Formal Approval. The Credit Committee/Investment Committee evaluates the overall risk of a potential transaction to determine if the financial institution should proceed with the transaction, and if so, under what conditions. The decision-making process should also factor in the environmental and social risk category, the findings of the environmental and social due diligence and any recommendations for corrective actions to mitigate potential environmental and social risk.

- Negotiation. After a financial institution decides to proceed with a transaction, the Loan Officers/Relationship Managers discuss and negotiate the terms and conditions with the client/investee. This may include requirements to comply with environmental and social parameters, such as implementing corrective actions to mitigate environmental and social risks.

- Disbursement. The Legal Department will develop the loan/investment agreement, which will stipulate the client’s/investee’s obligations for proceeding with a transaction to mitigate the financial institution’s exposure to potential risk. Additional stipulations in the legal agreement will include the client’s/investee’s obligations to comply with environmental and social parameters to minimize the financial institution’s exposure to environmental and social risk and liability.

- Monitoring. The financial institution monitors each transaction on a regular basis to ensure that the client/investee continues to comply with the conditions stipulated in the legal agreement. Any non-compliance, which increases the transaction’s overall risk, can be identified early on and followed up with the client/investee. Monitoring should also include a review of the client’s/investee’s ongoing environmental and social performance as well as implementation of corrective actions, as necessary, to identify early on a potential environmental and social risk to the financial institution.

Documentation and Recordkeeping

Documentation and record-keeping on environmental and social issues associated with each transaction are a key aspect of an effective ESMS.

This enables a financial institution to track the environmental and social performance of each transaction and to assess the financial institution’ s overall exposure to risk. As part of a financial institution’s existing recordkeeping process, the following documentation and records should be kept for each transaction:

Guidance for Managing E&S Risk

To help ensure that the ESMS is effective, a financial institution may need to prepare additional guidance documents for staff to have a better understanding of environmental and social issues and how to manage them.

As necessary or as identified during the review and continuous improvement process of the ESMS, a financial institution may decide to prepare guidance documents on the following:

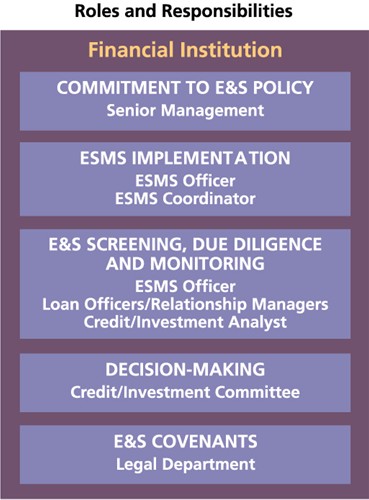

Roles, Responsibilities and Decision-Making

For a ESMS to function properly, it is essential that roles and responsibilities for carrying out the necessary procedures and making decisions are clearly defined.

Typically, the following staff of a financial institution are involved with implementing different aspects of the ESMS, although each financial institution should assign responsibilities in the manner that makes most sense according to its own structure:

- Senior Management, for example one or more representatives from upper management (for example a member of the Executive Board or the Fund Manager) should be responsible for the financial institution’s overall commitment to environmental and social objectives. Senior Management establishes the financial institution’s environmental and social requirements and conditions for clients/investees. In cases of unresolved environmental and social issues or non-compliance associated with a transaction that cannot be resolved by the Loan Officers/Relationship Managers, Senior Management determines the appropriate course of action to follow to reduce the financial institution’s potential exposure to environmental and social risk, which may include taking legal action against the client/investee.

- ESMS Officer is responsible for leading the financial institution’s effort to develop the ESMS as well as for communicating with senior management on environmental and social issues and concerns.

- ESMS Coordinator is responsible for developing and updating the procedures and documents that are part of the financial institution’s ESMS. This person also evaluates the environmental and social risks at the portfolio level and provides assistance to Loan Officers/Relationship Managers and Credit/Investment Analysts in evaluating and monitoring the environmental and social performance of clients/investees.

- Loan Officers/Relationship Managers are responsible for following the procedures of the ESMS at the transaction level. They discuss and negotiate possible environmental and social mitigation measures with the client/investee.

- Credit/Investment Analysts are responsible for evaluating the environmental and social risks at the level of individual transactions and make a recommendation to the Credit/Investment Committee on whether to proceed with a transaction.

- Credit/Investment Committee is responsible for deciding if E&S risks are acceptable to the financial institution’s overall exposure to risk before proceeding with a transaction.

- Legal Department ensures that the financial institution’s environmental and social requirements are incorporated in legal agreements for each transaction. The Legal Department may advise if a client’s/investee’s non-compliance with environmental and social clauses constitutes a breach of contract and is considered an Event of Default under the terms of the legal agreement that requires follow up by Senior Management.

Staff responsible for environmental and social risk management are encouraged to complete the Sustainability Training and E-learning Program (STEP), designed for managers and staff of financial institutions. This free, online training provides an understanding of sustainable finance and outlines how financial institutions can identify and manage environmental and social risks and environmental business opportunities.

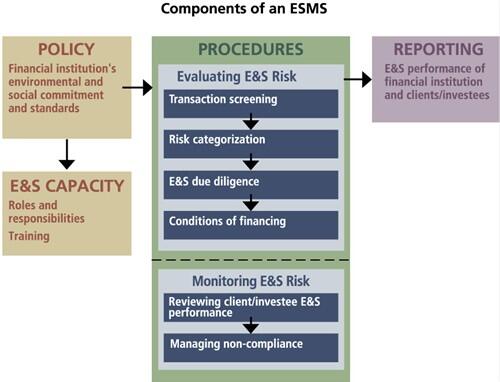

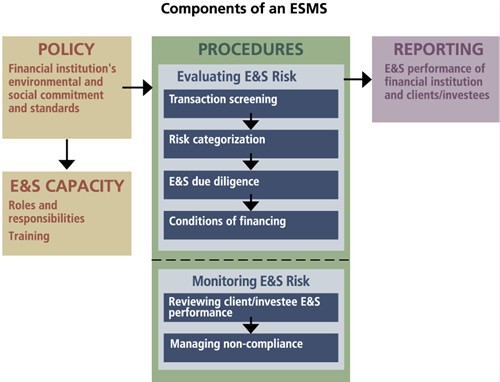

Components of an ESMS

An ESMS is anchored in a financial institution's environmental and social policy and depends on the environmental and social management capacity of its staff and, as applicable, external experts.

The ESMS includes the financial institution’s environmental and social policy and designated roles and responsibilities of its staff.

It is implemented through a set of procedures for:

- Screening transactions,

- Categorizing transactions based on their environmental and social risk,

- Conducting environmental and social due diligence,

- Decision-making process,

- Monitoring the client’s/investee’s environmental and social performance, and

- Managing a client’s/investee’s non-compliance with the financial institution’s environmental and social standards.

The procedures outlined in the ESMS should be applied to each transaction as part of a financial institution’s overall risk management framework. For each transaction, this also requires a financial institution to formally document its environmental and social review as part of its record-keeping process, consider environmental and social findings during the decision-making process, and incorporate environmental and social requirements such as a corrective action plan as clauses in legal agreements with clients/investee.

To ensure the effective implementation of the ESMS across operations, the financial institution needs to allocate the necessary resources for internal communication and training.

As part of its commitment to good corporate practices, a financial institution can periodically report on the environmental and social performance of transactions and measures taken to reduce overall exposure to environmental and social risk.

E&S Policy

A environmental and social (E&S) policy states a financial institution's vision and mission with respect to the environment, society and contributions to sustainable development.

It is a short, written statement that articulates the financial institution’s commitment to integrating environmental and social considerations into its business activities as well as contributions to sustainable development. It serves as the financial institution’s foundation within which the objectives and procedures of the ESMS are anchored.

E&S Standards

Commensurate with the environmental and social risk associated with clients/investees in its portfolio, a financial institution should define environmental and social standards that establish the E&S requirements for transactions.

Risk Categorization and Managing Portfolio Risk

To help a financial institution to determine the extent of environmental and social due diligence that will be required for a particular transaction, a environmental and social risk category should be assigned to each transaction.

The level of environmental and social risk will vary greatly for different types of financial transactions and by industry sectors. It can also be determined by factors such as scale and location and magnitude of potential environmental and social impacts.

Transaction Screening

At the initial stage of evaluating a potential financial transaction, financial institution staff should screen the activities of the potential client/investee to determine if it is an excluded activity or if there is a history of severe incidents.

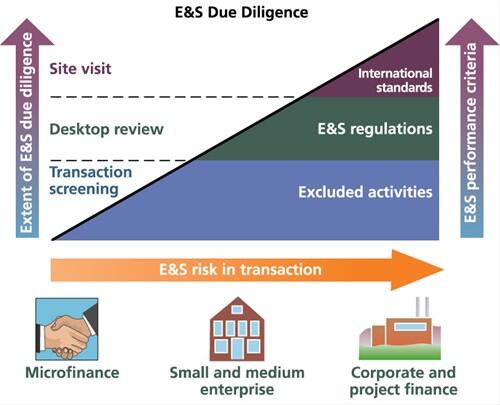

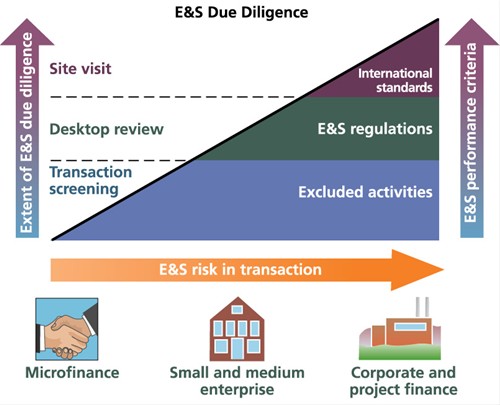

E&S Due Diligence

Conducting environmental and social (E&S) due diligence on transactions is a critical component of a financial institution's ESMS and its outcome should be factored in to the decision-making process for proceeding with a transaction.

The purpose of the environmental and social due diligence is to review any potential environmental and social risks associated with the business activities of a potential client/investee (not non-commercial/individual borrower) ensure that the transaction does not carry environmental and social risks, which could present a potential liability/risk to the financial institution.

Environmental and social due diligence involves the systematic identification, quantification and assessment/evaluation of environmental and social risks associated with a proposed transaction. This process also helps identify the mitigation measures that are necessary to reduce any environmental and social risks that are identified. The extent of the environmental and social due diligence and level of detail is based on the transaction’s environmental and social risk category and will vary by transaction type:

- Corporate finance

- Housing

- Insurance

- Leasing

- Microfinance

- Project finance

- Retail

- Short-term finance

- Small and medium enterprises

- Trade

The environmental and social due diligence can involve a simple desktop review or require a site visit with the use of technical experts, if necessary, to understand potential environmental and social risks associated with business activities and review a client’s/investee’s compliance with the financial institution’s environmental and social requirements.

The financial institution will need to develop the necessary guidance documents and checklists for use by financial institution staff in conducting the environmental and social due diligence. This should reflect the social and environmental issues that will be reviewed and other factors that will be considered to review compliance with the financial institution’s environmental and social requirements. A good starting point is a review of the environmental and social issues associated with those industry sectors that the financial institution is the most exposed to and the environmental and social laws as well as the specific context of the country in which clients/investees are located.

Desktop Review

Financial institution staff can conduct a desktop review, which involves reviewing documentation concerning environmental and social matters as they relate to a proposed transaction and the technical aspects of a client's/investee's operations.

This includes verifying compliance of the business activities of a proposed client/investee against the relevant environmental and social regulations as well as international standards, as necessary.

Due Diligence for Corporate Finance

The environmental and social risks associated with a corporate finance transaction will vary and can be significant depending on the operation's industry sector, size, location, and company commitment and capacity to managing environmental and social risks.

Due Diligence for Housing Finance

The environmental and social risks associated with housing finance may include inappropriate development location, poor building design (including inability to withstand natural disasters), inadequate construction, and unresolved land tenure issues.

Due Diligence for Insurance

The environmental and social risks associated with insurance transactions range from being minimal to significant, as a function of a client's operations or the complexity of the project (such as roads, dams, and mining operations).

The procedures and tools for conducting environmental and social due diligence for an insurance transaction are described in a financial institution’s Environmental and Social Management System and should include the following steps as part of a desktop review and a site visit if necessary:

Due Diligence for Leasing

The environmental and social risks associated with leasing activities are generally minimal for most transactions but will be more significant if the fixed asset involves the use of heavy equipment and as a function of the industry sector.

The procedures and tools for conducting environmental and social due diligence for leasing activities are described in a financial institution’s Environmental and Social Management System and should include the following steps as part of a desktop review and a site visit, if necessary:

Due Diligence for Microfinance

The environmental and social risks associated with a microfinance transaction are typically low partly due to the small size of the operation and the industry sector.

The procedures and tools for conducting environmental and social due diligence for microfinance are described in a financial institution’s Environmental and Social Management System.

Due Diligence for Project Finance

Due to the complexity, size, and location of operations such as roads, oil and gas explorations, dams, and power plants, which are financed as projects, these projects often have challenging environmental and social issues.

Challenging environmental and social issues may include involuntary resettlement, loss of biodiversity, impacts on indigenous communities, community and worker safety, pollution, contamination, and others. The life cycle of such projects generally includes several phases such as construction, operations, and decommissioning and typically extends over many years.

Due Diligence for Retail

The environmental and social issues associated with retail transactions that target individuals are generally non-existent.

However, for retail transactions there may be concerns associated with housing mortgage finance and potentially certain investment options that may involve controversial or high-risk projects/companies.

Due Diligence for Short-Term Finance

The environmental and social issues associated with a short-term finance transaction range from minimal to complex and vary according to size, industry sector, location, and company commitment to managing environmental and social risks.

Due Diligence for Small/Medium Enterprises

The environmental and social issues associated with financing small and medium enterprises can be quite significant and are primarily related to worker health and safety and pollution.

Generally, the environmental and social issues of small and medium enterprises are not closely monitored and the risks will vary depending on company size and its capacity to manage environmental and social risks, as well as by industry sector, and location.

Due Diligence for Trade Finance

The environmental and social risks of trade finance are associated with the production of those goods being traded and vary by industry sector and location.

The procedures and tools for conducting environmental and social due diligence for trade finance are described in a financial institution’s Environmental and Social Management System.

Corrective Action Plan

Financial institution staff may develop a corrective action plan with a timeframe for the client/investee to implement appropriate mitigation measures to comply with the financial institution's environmental and social requirements.

Depending on the nature of environmental and social risks associated with a client’s/investee’s operations, financial institution staff may develop a corrective action plan with a timeframe for the client/investee to implement appropriate mitigation measures to comply with its environmental and social requirements. The purpose of a corrective action plan is to mitigate potential environmental and social risks in the context of a transaction to an acceptable level for the financial institution.

E&S Covenants in Legal Agreements

Environmental and social (E&S) clauses can be incorporated into legal agreements with clients/investees. This helps reduce a financial institution's exposure to potential environmental and social risks associated with a client's/investee's.

Financial institution staff can incorporate environmental and social clauses into legal agreements with clients/investees to require clients/investees to comply with the financial institution’s environmental and social requirements. Doing so helps a financial institution reduce its exposure to the environmental and social risks associated with a client’s/investee’s operations throughout the lifetime of a transaction and gives the financial institution legal recourse in the case of non-compliance.

Monitoring Client/Investee E&S Performance

The purpose of monitoring a client's/investee's environmental and social performance is to assess existing and emerging environmental and social risks associated with a client's/investee's operations during the duration of a transaction.

Once a transaction has been approved, the financial institution needs to monitor the client’s/investee’s ongoing compliance with the environmental and social clauses stipulated in the legal agreement. Environmental and social risks or compliance status may change from the time of transaction approval.

Managing Non-Compliance

In cases of a client's/investee's non-compliance with the financial institution's environmental and social standards that are stipulated in the legal agreement, the client/investee will have a timeframe for resolving the issue.

During monitoring, financial institution staff may identify environmental and social issues, such as a client’s/investee’s non-compliance with one or more of the clauses stipulated in the legal agreement.

Internal and External Reporting

A financial institution's ESMS should include periodic reporting on the environmental and social performance of transactions and measures taken to reduce its overall exposure to environmental and social risk.

Financial institution staff should compile all environmental and social findings from monitoring clients/investees and aggregate findings at the portfolio level. By analyzing this information, the financial institution can have a better understanding of its overall exposure to environmental and social risk through its portfolio.

Implementing an ESMS

Once the ESMS has been developed and formally approved by Senior Management, it can be institutionalized and rolled out across the financial institution.

Once the ESMS has been developed and formally approved by Senior Management, it can be institutionalized and rolled out across the financial institution.

Assign ESMS Responsibilities

The ESMS lists the roles and responsibilities needed for effective implementation of environmental and social risk management procedures.

Additional responsibilities for environmental and social risk management should be assigned to existing staff or new staff should be hired as required by the ESMS.

ESMS Review and Continuous Improvement

The ESMS should be updated regularly to reflect any changes in the environmental and social regulations and/or international best practices that affect the business operations of a financial institution's clients/investees.

ESMS Testing Phase

The ESMS should be implemented gradually, starting with a pilot test phase with limited application (for example, at one branch or limited to a specific sector or a certain aspect of the financial institution's financial activities).

Internal Communication and Training

The purpose of the ESMS and its supporting procedures should be communicated to all staff of a financial institution. This can be achieved through an office memo or emails, staff meetings, newsletters, presentations and seminars.

Review E&S Regulatory Framework

A financial institution needs to be knowledgeable of the environmental and social laws of the country in which it operates, to be able to verify how its commercial clients/investees comply with applicable environmental and social laws, which vary by country.

As part of its environmental and social due diligence process, a financial institution may verify how its commercial clients/investees comply with applicable environmental and social laws, which vary by country.

IFC E&S Requirements

IFC requires financial institution (FI) clients to manage environmental and social risks in their portfolio while encouraging them to expand product offerings into financing/lending to sustainable energy projects.

Sustainability is about ensuring long-term business success while contributing toward economic and social development, a healthy environment, and a stable society. IFC’s definition of sustainability as applied to financial institutions encompasses the following dimensions of good business performance:

Implementing IFC E&S Requirements

The International Finance Corporation (IFC) strives for positive development outcomes in the private sector projects - including financial institutions - it finances.

Designate an ESMS Officer

The financial institution is required to nominate an officer to serve as the person with the responsibility of overall administration and oversight for the implementation of the ESMS.

Establish and Maintain an ESMS

A financial institution is required to establish a Environmental and Social Management System to manage risks in a manner consistent with IFC's Policy on Environmental and Social Sustainability and IFC's Environmental and Social Review Procedure.

Develop an ESMS

A financial institution may be required to develop a Environmental and Social Management System to identify and manage the risks and impacts associated with its financing activities.

Based on IFC’s review, a financial institution may be required to develop a Environmental and Social Management System (ESMS) to manage the risks and impacts associated with its financing activities in order to ensure that these comply with the IFC Exclusion List, applicable national environmental and social regulations and the IFC Performance Standards.

Enhance an Existing ESMS

Based on IFC's review, a financial institution may be required to enhance its existing risk management procedures for assessing environmental and social risks and meet IFC's standards

Based on IFC’s review, a financial institution may be required to modify its existing risk management procedures for assessing environmental and social risks to meet IFC’s standard for a Environmental and Social Management System (ESMS) as well as applicable IFC environmental and social performance requirements. To enhance its existing capacity for managing environmental and social risks, the financial institution may be required to:

IFC E&S Performance Requirements

The financial institution's Environmental and Social Management System should be designed to manage and reduce its overall exposure to environmental and social risk.

Applicable National E&S Laws

The non-compliance of a commercial client/investee with applicable environmental and social laws may present a potential risk to the financial institution.

To manage the risk associated with non-compliance of a commercial client/investee with applicable environmental and social laws, financial institutions should avoid financing a commercial client/investee whose activities do not comply with applicable national environmental and social laws unless the client/investee agrees to a corrective action plan.

IFC Exclusion List

The IFC Exclusion List defines the types of projects that IFC does not finance, either directly or indirectly through financial institution clients.

IFC Performance Standards

When the potential environmental and social impacts associated with a financial institution's client/investees are significant, the financial institution should apply the IFC's Performance Standards as a benchmark for identifying and managing these risks.

The IFC Performance Standards are an international benchmark for identifying and managing environmental and social risk and has been adopted by many organizations as a key component of their environmental and social risk management. IFC’s Environmental, Health, and Safety (EHS) Guidelines provide technical guidelines with general and industry-specific examples of good international industry practice to meet IFC’s Performance Standards.

IFC E&S Requirements for FI Clients

By applying a comprehensive set of environmental and social performance standards to projects, IFC expects to achieve environmental and social sustainability, which represents an important component of positive development outcomes of projects.

Through its Policy on Environmental and Social Sustainability, IFC puts into practice its commitment to environmental and social sustainability. This commitment is based on IFC’s mission and mandate, which is to promote sustainable private sector development in developing countries, helping to reduce poverty and improve people’s lives. IFC believes that sound economic growth, grounded in sustainable private investment, is crucial to poverty reduction. Translating this commitment into successful outcomes depends on the efforts of IFC and its clients.

Report Annually

All IFC clients including financial institutions are required to report to IFC on an annual basis on their environmental and social performance from disbursement until the end of the IFC investment.

Reporting for Banking Institutions

Banking institutions that are IFC clients are required to report to IFC on an annual basis on their environmental and social performance by submitting an Annual Environmental Performance Report (AEPR).

As part of IFC’s annual reporting requirements, Banking Institutions are required to provide information on:

Reporting for Leasing Companies

Leasing Companies that are IFC clients are required to report to IFC on an annual basis on their environmental and social performance by submitting an Annual Environmental Performance Report (AEPR).

As part of IFC’s annual reporting requirements, Leasing Companies are required to provide information on:

Reporting for Microfinance Institutions

Microfinance institutions that are IFC clients are required to report to IFC on an annual basis on their environmental and social performance by submitting an Annual Environmental Performance Report (AEPR).

As part of IFC’s annual reporting requirements, Microfinance Institutions are required to provide information on:

Reporting for Private Equity Funds

Private equity funds that are IFC clients are required to report to IFC on an annual basis on their environmental and social performance by submitting an Annual Environmental Performance Report (AEPR).

As part of IFC’s annual reporting requirements, Private Equity Funds are required to provide information on:

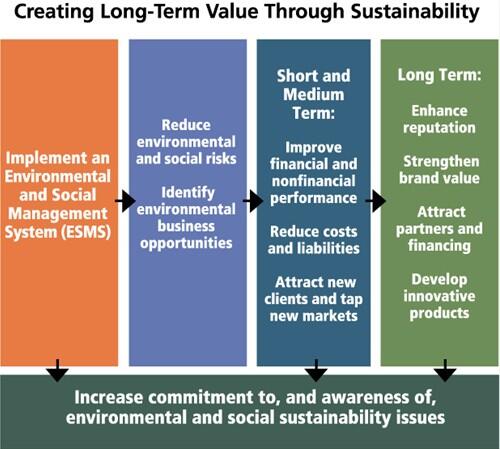

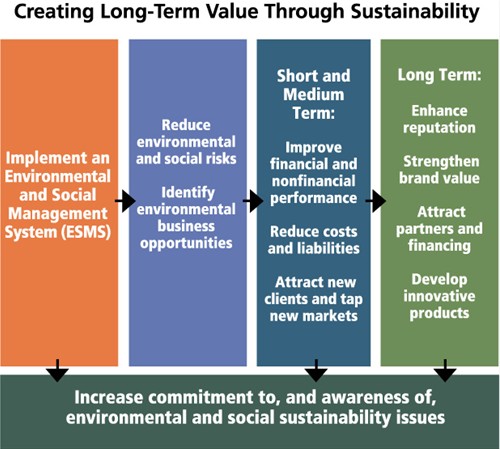

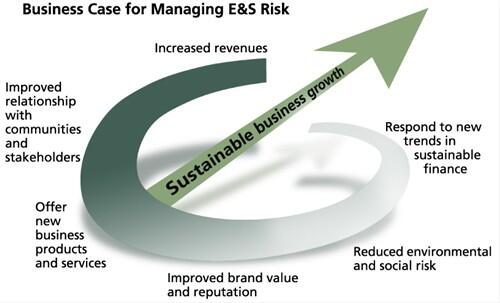

Business Case for Managing E&S Risk

Considering environmental and social risks as part of the risk appraisal process for transactions helps a financial institution to decrease its exposure to overall risk and contributes to its long-term financial viability.

A financial institution can do so by developing a Environmental and Social Management System, which can be integrated into its existing risk management framework including the risk appraisal process for transactions. A well-developed Environmental and Social Management System can lead to decreased exposure to environmental and social risks, increased market opportunities, and enhanced reputation, which help contribute to the long-term financial viability of financial institution.

There is a clear business case for financial institutions to establish a management system that incorporates environmental and social risks into their overall approach to risk management. If environmental and social risks are considered too high or cannot be mitigated to an acceptable level, financial institutions can decide not to engage in a financial transaction, even if otherwise it is projected to have a good financial return. Similarly, financial institutions can add value to their clients or investees by helping identify and mitigate E&S risks that could threaten the viability or profitability of their business.

An increasing number of financial institutions are voluntarily adopting international environmental and social standards to identify and mitigate E&S risks, also creating opportunities and harmonizing the requirements for environmental and social sustainability for their clients/investees. These standards facilitate the unique role that financial institutions can play in promoting sustainable development outcomes.

Addressing E&S Risk

Understanding and managing environmental and social risks is becoming increasingly recognized as an important element of a financial institution's approach to risk management.

Benefits of Addressing E&S Risks

Environmental and social risk management benefits a financial institution by improving overall risk management, identifying new environmental business opportunities, and adding value to clients and investees, thus gaining a competitive advantage.

More and more financial institutions are now convinced that environmental and social risks of clients need to be considered and that this can be done effectively by incorporating environmental and social risk into risk management processes.

In recent years, financial institutions – in particular those that are operating at the international level or have positioned themselves as “sustainable” or “green” – have developed a ESMS and associated policies and procedures because they see the strong business case for E&S risk management.

Some financial institutions continue to be uncertain about the importance and benefits of addressing environmental and social risk. A few financial institutions, such as those that operate in smaller markets or engage in financial transactions with low perceived environmental and social risk, may argue that a Environmental and Social Management System (ESMS) is not relevant to their financial performance or that it increases transaction costs without bringing financial benefits. Also, some financial institutions may feel that environmental and social risk management provides no value-added to their portfolio and consider “green” markets as niche products in which their clients/investees are not interested.

Regardless of the size or type of financial institution, the type of financial transactions involved and the market in which it operates, a financial institution can benefit from environmental and social risk management by using it to improve its overall risk management, identify new environmental business opportunities, and add value to their clients and investees, thus gaining a competitive advantage.

Better Risk Management

Financial institutions are directly exposed to credit, liability and reputational risks arising from E&S issues associated with their clients'/investees' operations.

Competitive Advantage

Good governance, accountability and increased lender liability are relevant to financial institutions. Clients/investees are starting to look at a financial institution's position on environmental and social issues when deciding where to take their business.

Case Studies

Case Studies

Small and Medium Enterprise Finance

Loans to a Cotton Producers Cooperative in Brazil

Financing SMEs creates high developmental impact and is considered to have lower environmental and social (E&S) risks than project and corporate finance because of SMEs’ smaller footprint. However, unlike larger corporations, SMEs can have limited capacity and resources to manage E&S risks, and authorities may in some cases not regulate and monitor them as closely.

Project Finance Gone Wrong

Electricity Transmission in Southeast Nigeria

Environmental and social due diligence (ESDD) assessment is a critical component of a financial institution’s environmental and social (E&S) management system. Reviewing consultation and communication with communities can help identify and avoid potential problems.

Integrating Environmental and Social Risk Management into a Financial Institution's Overall Operations

Environmental and social (E&S) risk management is often treated as a separate consideration for many organizations, including some financial institutions. Because E&S risks aren’t as easily quantified as financial risks (which can be assigned a score), they can be hard to include in a financial institution’s models and decision-making. Many E&S risk management approaches are based on project and transaction risks rather than overall client risk, which works for some project and asset-based corporate finance transactions. However, when banks and other companies have multiple transactions and products with the same client, a more integrated and holistic approach can make more sense. Know Your Client (KYC) is often a good approach for integrating E&S risks into an organization’s overall decision-making and for dealing with multiple transactions and products for the same client.

Corporate Finance

Forestry Products in Papua New Guinea

An international bank provided a six-year $100 million corporate loan to support the growth and expansion of a well-established paper and pulp operation in Papua New Guinea, whose plantations and mill provide paper products for export. Because of a significant, increased demand for the company’s paper products (linked to a decline in single-use plastics), the company acquired adjoining blocks of land for expansion and obtained the necessary local approvals and permits for the expansion, including permits for felling existing trees. On receiving the financing, the company proceeded with its aggressive expansion plan that included harvesting existing timber and replanting with a faster-growing species.

Venture Capital

Business-to-Consumer Delivery in Indonesia

A venture capital firm made an early investment in a company providing business-to-consumer delivery in Indonesia through a new tech platform. The platform offered consumers a wide range of products they could order through an app that connected them to retailers and handled the ordering and payment process. The retailers then packed the goods for third-party drivers to pick up and deliver. These drivers--a key component of the business model--were independent contractors who signed-up for the work and used their own vehicles for the deliveries.