Sustainable Banking and Finance Network (SBFN)

Established in 2012, the Sustainable Banking and Finance Network (SBFN) is a voluntary community of financial sector regulators, central banks, ministries of finance, ministries of environment, and industry associations from emerging markets committed to advancing sustainable finance and responsible investment for national development priorities, financial market deepening, and stability.

Sustainable Banking and Finance Network Meetings

The SBFN Global Meetings hosted since 2012 are the principal space for dialogue, networking and knowledge generation among SBFN members. These meetings provide SBFN members with a platform from which to showcase national and regional initiatives in the sustainable finance space, and to explore approaches from different markets. Furthermore, these meetings provide the opportunity to discuss current issues and jointly develop new approaches to sustainable banking.

Sustainable Banking Guidance from SBFN Members

As of November 2021, 33 SBFN countries had launched over 200 national framework documents to support sustainable finance. The process of developing and implementing these frameworks generates a positive dynamic between the public and private sector, enabled by SBFN’s mix of both regulators and industry associations. This is seen in the mix of market-based actions and policy leadership that is resulting in more effective frameworks and implementation.

Sustainable Banking and Finance Network - Contact Information

The secretariat of the Sustainable Banking and Finance Network is hosted by the International Finance Corporation.

Please contact us for additional information, questions and feedback.

Rong Zhang

Senior Policy Officer

Environment, Social and Governance Department

International Finance Corporation

2121 Pennsylvania Ave., NW

Washington, DC 20433

E-mail:

rzhang [at] ifc.org (rzhang[at]ifc[dot]org)

sbn [at] ifc.org (sbn[at]ifc[dot]org)

Sustainability Frameworks

Investors are increasingly realizing that environmental, social and corporate governance issues can impact the performance of investment portfolios. Sustainability frameworks have been developed to help organizations manage these issues.

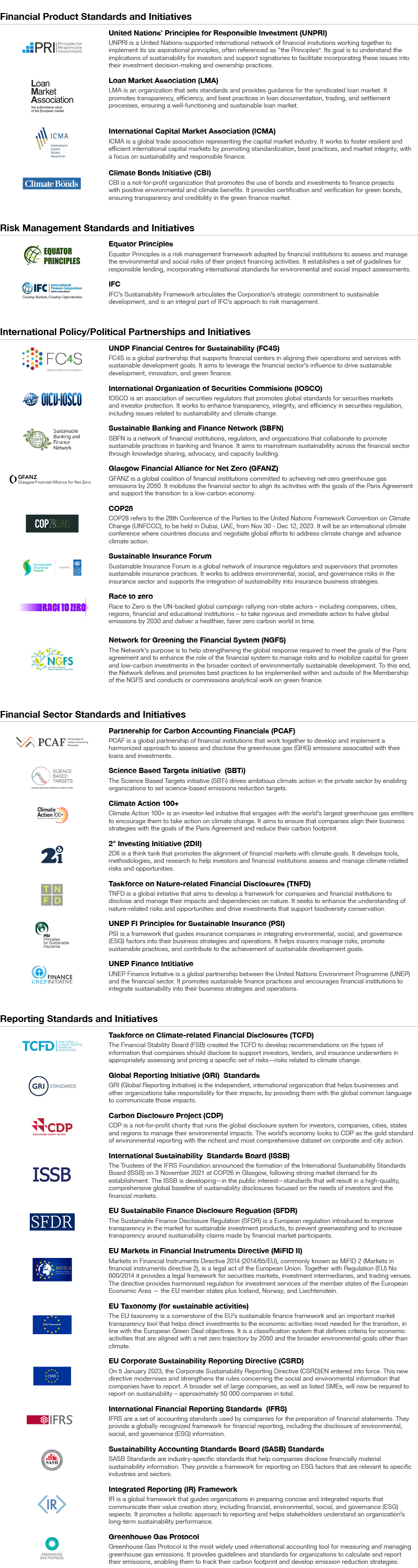

Equator Principles

The Equator Principles are a voluntary set of environmental and social guidelines for project finance lending.

They provide a framework for financial institutions to manage environmental and social issues related to projects they finance anywhere in the world and to all industry sectors, including mining, oil and gas, and forestry. The Equator Principles are based on IFC’s Performance Standards and apply to projects that exceed $10 million.

United Nations Financial Initiative

In recognition that the financial sector has a valuable contribution to make in protecting the environment while maintaining the health and profitability of their businesses, the United Nations Environment Programme (UNEP) joined forces with a group of commercial banks and launched the Banking Initiative.

United Nations Principles for Responsible Investment

In 2005, 20 institutional investors from 12 countries accepted an invitation from the Secretary General of the United Nations to participate in an Investor Group to jointly develop the Principles for Responsible Investment (PRI).

Supported by experts from the investment industry, governmental organizations, civil society and academia, the Investor Group formulated the following principles:

Sustainability Reporting

Communicating a financial institution's performance in sustainability initiatives and environmental and social management is a key component in creating long-term value.

Paris Agreement

What is Paris Agreement

The Paris Agreement (PA) is a legally binding international treaty on climate change. It was adopted by 196 Parties at COP 21 in Paris, on 12 December 2015 and entered into force on 4 November 2016. Since then, 197 countries – nearly every nation on earth – have endorsed the Paris Agreement.

Focus of the Paris Agreement:

-

Keep global warming "well below" 2°C above pre-industrial times and continue all efforts to limit the rise in temperatures to 1.5°C

-

Aim for rapid reductions of GHG emissions - known as net zero - between 2050 and 2100 to achieve a balance between emissions from human activity and the amount that can be captured by GHG “sinks”

-

Each country to set its own emission-reduction targets, reviewed every five years to raise ambitions

-

Rich countries to help poorer nations by providing funding, known as climate finance, to adapt to climate change and switch to renewable energy.

The Paris Agreement’s central aim is to strengthen the global response to the threat of climate change by keeping a global temperature rise this century well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 °C.

Source: WRI Global Risks Report 2022

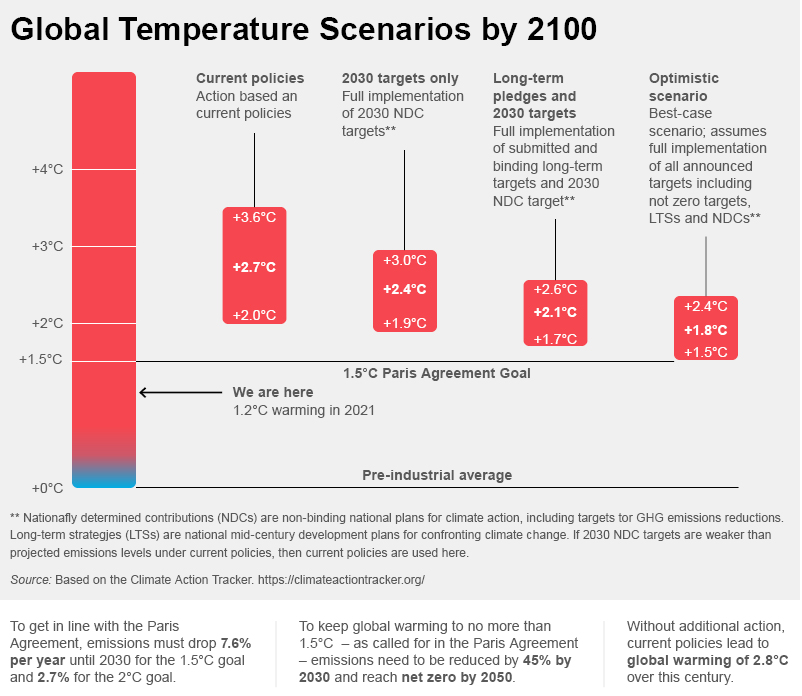

To get in line with the Paris Agreement, emissions must drop 7.6% per year until 2030 for the 1.5°C goal and 2.7% for the 2°C goal.

To keep global warming to no more than 1.5°C – as called for in the Paris Agreement – emissions need to be reduced by 45% by 2030 and reach net zero by 2050.

Without additional action, current policies lead to global warming of 2.8°C over this century.

Why Paris Agreement Matters

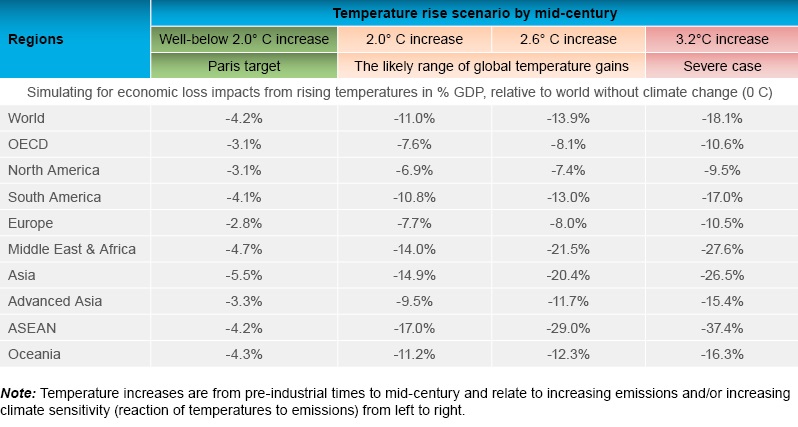

Global temperature rises will negatively impact GDP in all regions by mid-century. The current trajectory of temperature increases, assuming action with respect to climate change mitigation pledges, points to global warming of 2.0–2.6°C by midcentury. The loss in global economic value in this scenario could be up to 10% higher than if the Paris Agreement of much less than 2°C rise in temperatures is reached. Economies in southeast Asia (ASEAN) countries would be hardest hit. In a severe scenario of a 3.2°C-rise in temperatures, the global GDP loss could be as much as 14% higher than that under the Paris targets.

Source: Swiss Re Institute: The economics of climate change: no action not an option

The Financial Stability Board estimates the total global stock of manageable assets at risk from climate change to be as high as US$43tn by the end of the century1.

1 TCFD (2017) Recommendations of the Task Force on Climate-related Financial Disclosures. London: Financial Stability Board.

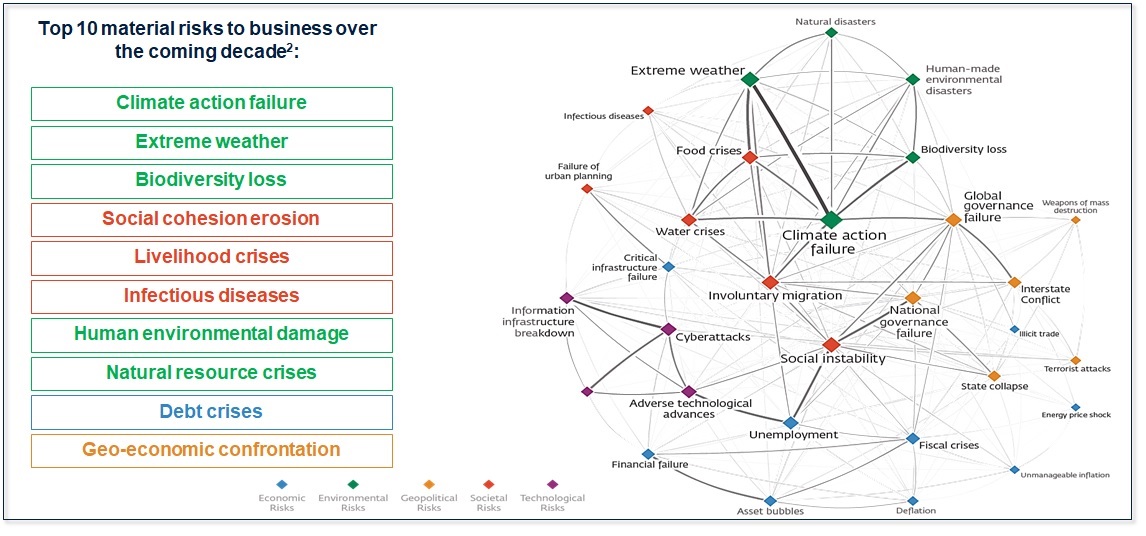

2 WEF (World Economic Forum) (2020) The Global Risks Report 2020. Geneva: WEF.

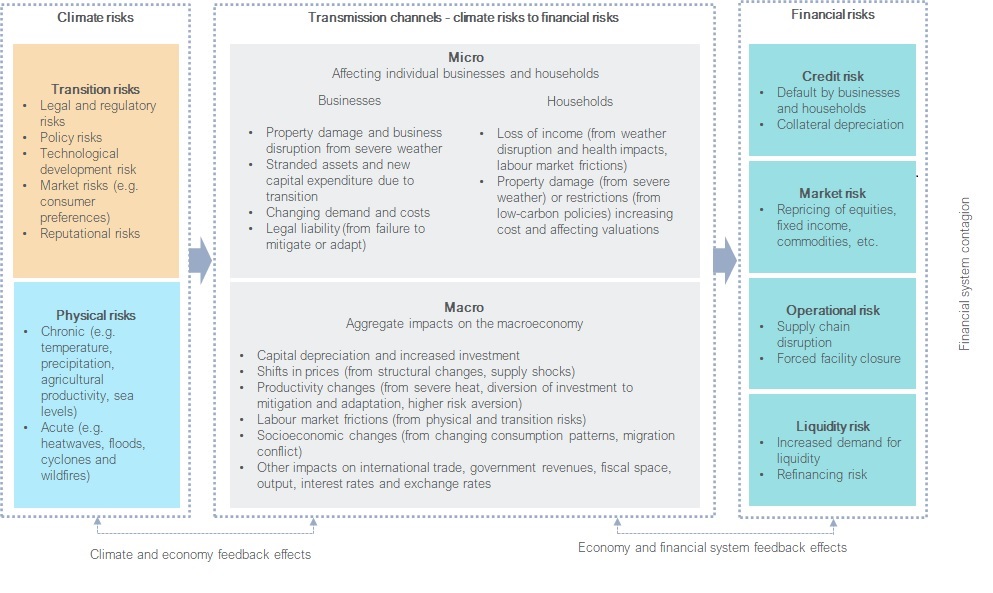

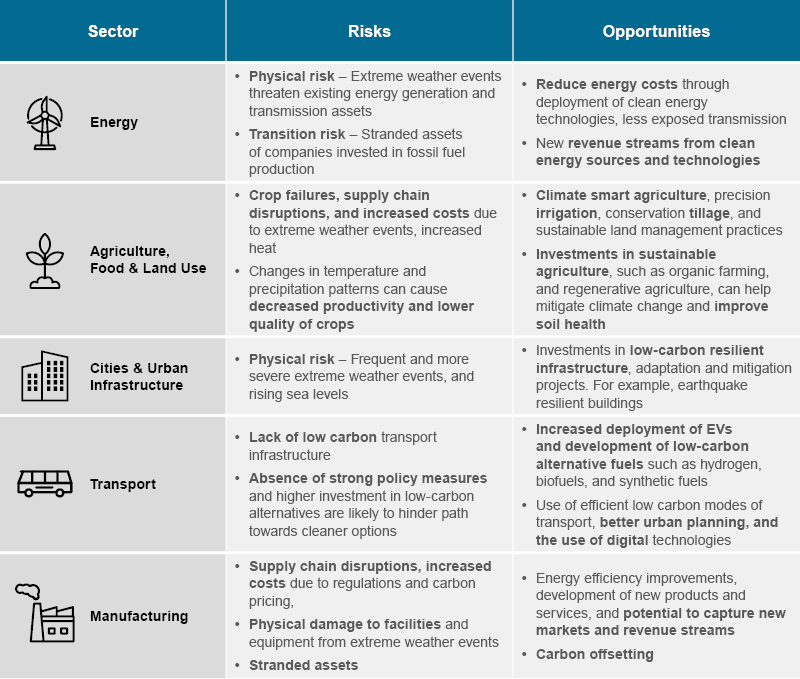

Climate risks could affect the economy and financial system through a range of different transmission channels.

Climate Risks and Opportunities for Financial Institutions

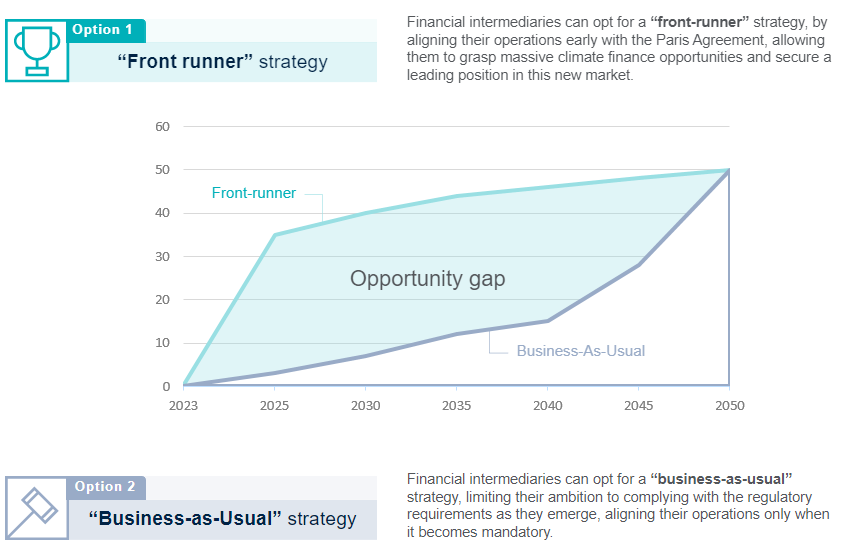

Paris alignment will strengthen relationships with all the stakeholders that banks need for long-term viability and success. All banking stakeholders expect to undergo changes towards more sustainable approaches.

There is a short-term commercial case for Financial Institutions for early alignment with the Paris Agreement. As new regulatory requirements emerge, the alignment of operations is just a matter of time, but the opportunities arising from an early adoption are significant and will be leveraged by those willing to adapt now.

Many banks are already accelerating their transition to secure “front-runner” market positioning in the emerging markets. The following Banks have taken part in the UNEP FI’s TCFD program.

- Climate change has emerged as one of the biggest systemic risks to the financial markets, but it also presents a major opportunity and one that will reshape the markets.

- At least USD 4.3 trillion in annual finance flows or a 20% year-on-year increase by 2030 is required to avoid the worst impacts of climate change.

-

Aligning finance with a 1.5°C path would demand to cut the financing of high emissions activities and some resources to be reallocated to climate finance.

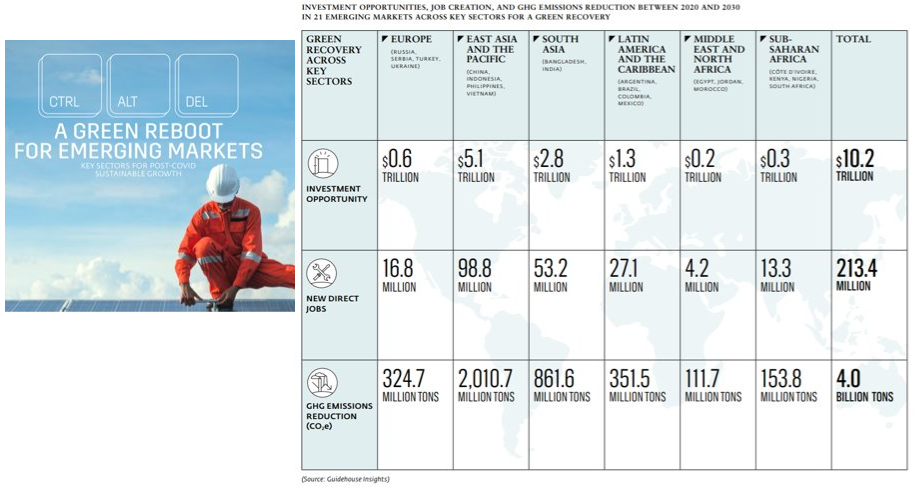

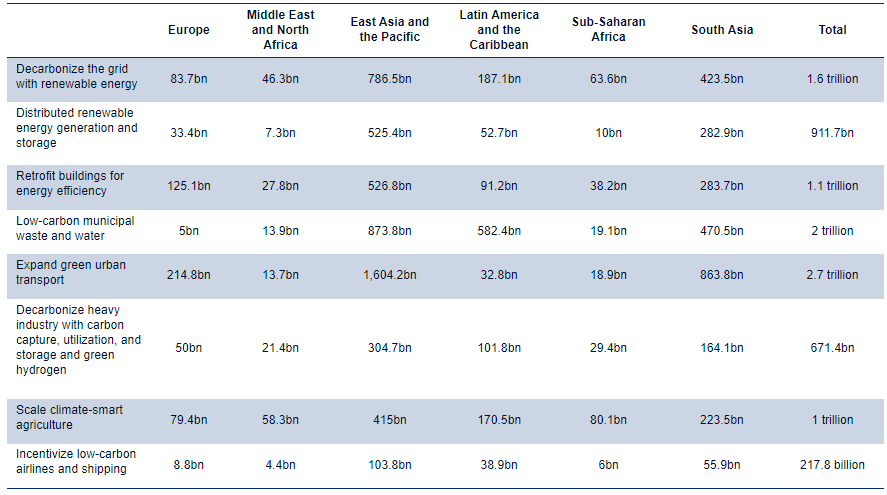

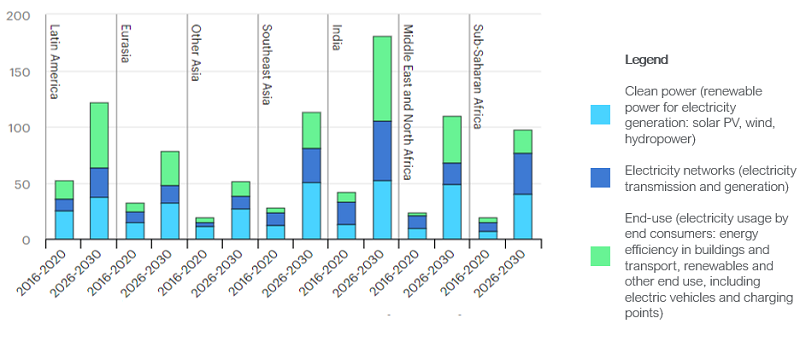

IFC’s analysis of the 21 major emerging-market economies that represent 62 percent of the world’s population and 48 percent of global emissions have shown that focusing on green investments in ten key sectors between 2020 and 2030 could generate $10.2 trillion in climate investment opportunities and reduce CO2 by 4 billion tons.

Climate investment opportunities in 10 key sectors by region.

Investment levels in clean energy will grow dramatically across all emerging markets. Current vs. future scenarios average annual investment in clean power, grids and energy end use by emerging markets and developing economies in climate-driven scenarios, 2016-2030 (USD Billion)

Regulations and Initiatives

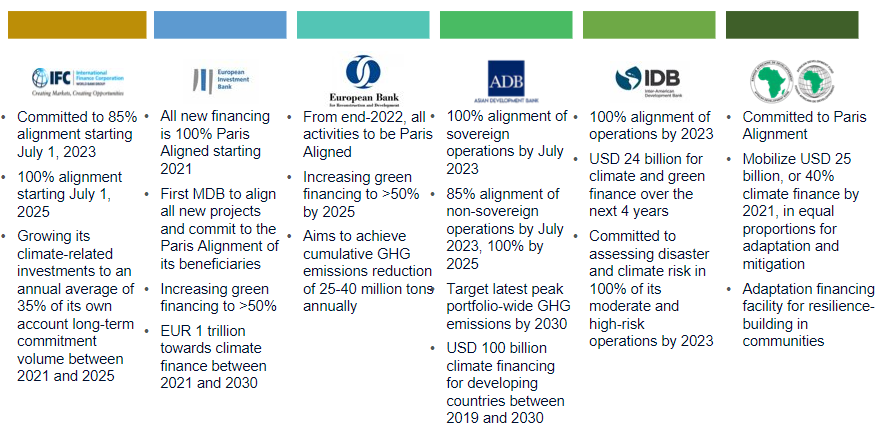

In 2017, MDBs committed to align their financial flows with the goals of the Paris Agreement, and at COP24 they published their Joint Approach, to put that commitment into action. The Joint MDB framework guides each MDB as it develops its own system.

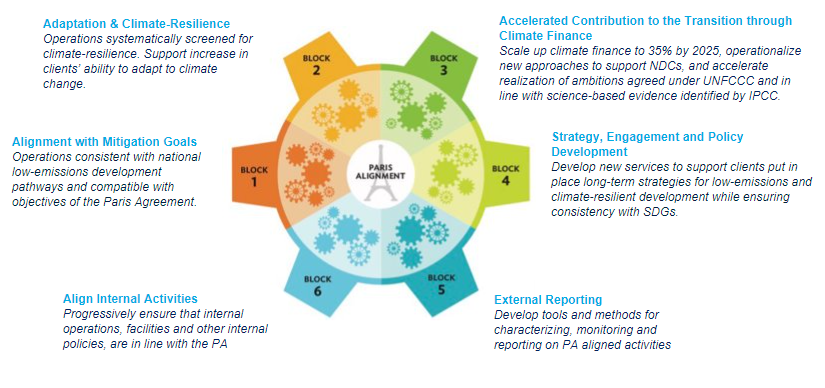

The MDBs’ approach is based on six building blocks that have been identified as the core areas for alignment with the objectives of the Paris Agreement. A joint MDB working group continues to develop methods and tools to operationalize this effort under each of the building blocks. These building blocks serve as the basis for a joint MDB approach towards alignment with the objectives of the Paris Agreement, while fully acknowledging each MDB’s mandate, capability and operational model. Accordingly, differentiated ways and timing of implementation are possible within robust common principles, framework, criteria and timeline.

Source: Joint Declaration MDBs Alignment Approach to Paris Agreement at COP24.

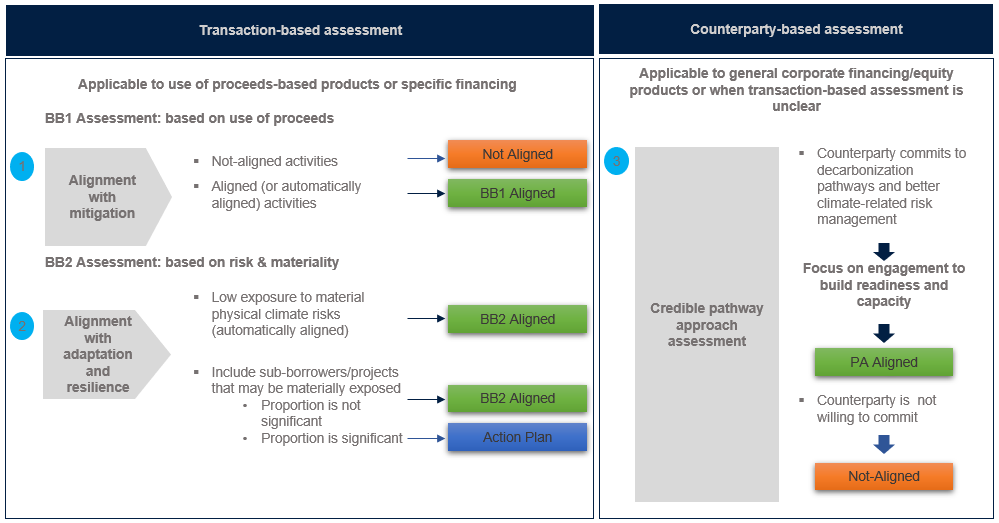

MDBs’ Paris Alignment Framework for Financial Intermediaries.

Operations should not have a material impact on climate change and should be consistent with low-emission development pathways and compatible with Paris Agreement.

A number of policies and initiatives have been developed around the world to support the goal of the Paris Alignment to align financial flows.

Source: Climate Action Tracker, PwC internal resources, AfDB, European Commission, European Parliament, US International Trade Administration

Public and private initiatives in areas of sustainability relevant to the financial sector have exponentially grown over the last decade.

Additional Resources

Below are some additional resources that could be useful.

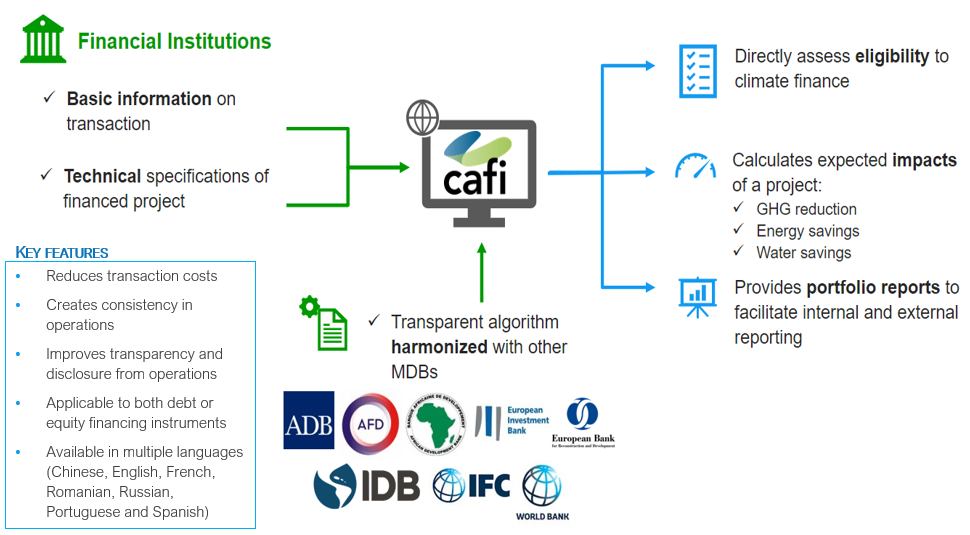

CAFI

CAFI or Climate Assessment for Financial Institutions tool, is a first-of-its-kind leading impact monitoring and reporting tool developed by IFC for climate impact data evaluation. It is a digital, web-based platform that helps financial institutions assess the climate eligibility of their portfolio and measure its development impact.

CAFI or Climate Assessment for Financial Institutions tool, is a first-of-its-kind leading impact monitoring and reporting tool developed by IFC for climate impact data evaluation. It is a digital, web-based platform that helps financial institutions assess the climate eligibility of their portfolio and measure its development impact.

|

|

IFC GBAC is a knowledge initiative for banks to support their transformational journey towards green banking. The initiative was launched in the ECA region in 2021 and replicated in the Africa region in 2022. |

|

|

In 2018, IFC launched the Green Bond Technical Assistance Program (GB-TAP), an IFC-managed and administered program, to create a market for green bonds in developing countries. GB-TAP provides technical assistance on green bond issuances and delivers global public goods through a range of activities and initiatives. |

|

|

Alliance for Green Commercial Banks (the Alliance) is a global initiative that brings together financial institutions (FIs), research institutions, and innovative technology providers to develop a green community in emerging markets to collectively finance the infrastructure and business solutions needed to urgently address climate and environmental risks. |

Current Cornerstone Banks: Bank of China (Hong Kong), Citi, Crédit Agricole CIB, HSBC, and Standard Chartered

Partnerships: The Alliance’s Partnership structure includes Global Partners and Knowledge Partners Current Partners The Carbon Trust, The Institute of Public Environmental Affairs, and China National Institute of Standardization, and University of Chicago.

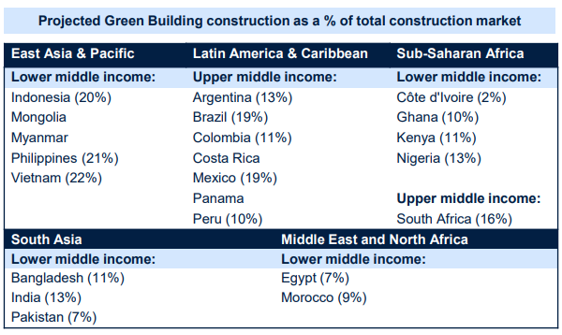

Market Accelerator for Green Construction (MAGC) In 2018, IFC and the UK Government’s Department for Business, Energy and Industrial Strategy (BEIS) forged a partnership to combat climate change in developing countries by crowding in public and private sector financing for certified green buildings. By accelerating the construction of certified green buildings, the program aims to mobilize $2 billion in investments to help mitigate climate change.

Geographic Scope of the Program

By combining information on the GHG reduction potential combined with IFC’s in-country knowledge, including market intelligence on the investment opportunities in developing and emerging countries, the country prioritization exercise identified the following list of countries:

- Latin America & Caribbean: Argentina, Brazil, Colombia, Costa Rica, Mexico, Panama, Peru

- Sub-Saharan Africa: Cote d’Ivoire, Ghana, Kenya, Nigeria, South Africa

- Middle East and North Africa: Egypt, Morocco

- South Asia: Bangladesh, India, Pakistan

- East Asia: China (advisory only), Indonesia, Mongolia, Myanmar, Philippines, Vietnam.

International Conventions and Standards

The activities of clients/investees may be regulated under international conventions and subject to various international sustainability and certifications. A financial institution should be knowledgeable of which of these apply to their clients/investees.

International Conventions and Agreements

The activities of a financial institution's clients/investees may be regulated under international conventions, agreements and bans.

International conventions, agreements and bans have been adopted by governments around the world in the following areas:

International Standards

Various international sustainability standards and industry certifications have been established, which may apply to a financial institution's client/investee.

International industry certifications have been established, for example, for managing the world’s forests and fisheries, encouraging businesses to market products and services that are kinder to the environment, improving the global supply chain, and reducing the environmental impact of production sites.

Regional Initiatives

European Union (EU) Initiatives

Sustainable Finance Disclosure Regulation (SFDR) is a European regulation introduced to improve transparency in the market for sustainable investment products, to prevent greenwashing and to increase transparency around sustainability claims made by financial market participants. The SFDR is a fundamental pillar of the EU Sustainable Finance agenda, having been introduced by the European Commission as a core part of its 2018 Sustainable Finance Action Plan, which also include the Taxonomy Regulation and the Low Carbon Benchmarks Regulation.

EU Taxonomy Regulation is a classification system that helps companies and investors identify “environmentally sustainable” economic activities to make sustainable investment decisions. Environmentally sustainable economic activities are described as those which “make a substantial contribution to at least one of the EU’s climate and environmental objectives, while at the same time is not contrary to Do Not Significant Harm (DNSH) principle and meets minimum safeguards.”. Recently, partnership between IFC and the Equator Principles Association has brought important research that explores linkages and provides practical comparisons between the EU Taxonomy’s DNSH and minimum safeguards requirements, and the IFC Performance Standards and World Bank Group Environmental, Health, and Safety (EHS) Guidelines. Link: https://www.ifc.org/en/insights-reports/2023/publications-ifceutaxonomy

Ghanaian Sustainable Banking Principles

Sustainability In The Ghana Financial Sector

With the environmental and social challenges faced by societies today, conventional business models that do not consider the triple bottom line of people, profit and planet are likely to be unsustainable and uncompetitive. Globally, the financial sector plays a key role in the sustainability conversation and it has introduced various initiatives to encourage integration of environmental and social considerations into financing decisions.

New business opportunities and portfolios are also an outcome of the sustainable finance agenda and various financial entities have seized the opportunity to expand their portfolios to include green finance instruments such as green bonds, renewable energy and energy efficiency financing, green buildings and green mortgages.

In Ghana, the sustainable finance agenda is pioneered by the Bank of Ghana, and the Ghana Association of Bankers, which have developed a customized framework on sustainable banking for the Ghanaian banking sector. Other financial service regulators must play a key role in promoting the sustainable finance agenda in Ghana. They are currently in various discussion phases aimed at creating agendas that key into the global conversations on sustainable finance.

- Overview of the Ghanaian Banking Sector

-

The Ghanaian Financial Sector contributes approximately 6.5% to Ghana’s GDP, with an estimated total banking sector asset of GHC 107.34 billion – as at December 2018. The Financial sector is overseen by the BOG, the regulatory body established by the 1957 Bank of Ghana ordinance. The BOG has supervisory and regulatory authority in banking and non-bank financial business activities.

The banking sector underwent some reforms in 2017 and 2018 including the recapitalization efforts by the Bank of Ghana which required banks to meet up with a minimum paid up capital requirement of GHC400million (USD72 million. Following the recapitalization, the number of licensed banks went from thirty-four (34) to twenty-three (23). In addition, there are 319 microfinance institutions, 135 rural banks and 40 non-banking financial institutions.

There are three categories of banking licenses for operating in the sector:

- Class I Universal banking license – this allows the holder to transact domestic banking business (this was previously the UBBL)

- Class II Banking License – this allows the holder to conduct banking or investment banking business with non-residents and other class II banking license holders in currencies other than the Ghanaian Cedi (unless otherwise permitted by the BOG.

- General banking license – this allows both the Class I and II banking business in and from within Ghana

The convening national platform for the sector is the Ghana Association of Bankers (GAB).The association’s objectives include:

- Creating an avenue for representation on issues pertaining to economic, fiscal, monetary and other matters affecting the performance of the financial system

- Providing a platform for the sector to express its views on regulatory legislative initiatives

- Carrying out research, analysing and disseminating information on issues affecting the sector

- Enhancing sector performance

- Participating and contributing to the activities of the West African Bankers Association

The Ghana Association of Bankers has played a key role in the Sustainable Banking Principles since the onset.

- The Ghanaian Sustainable Banking Principles

-

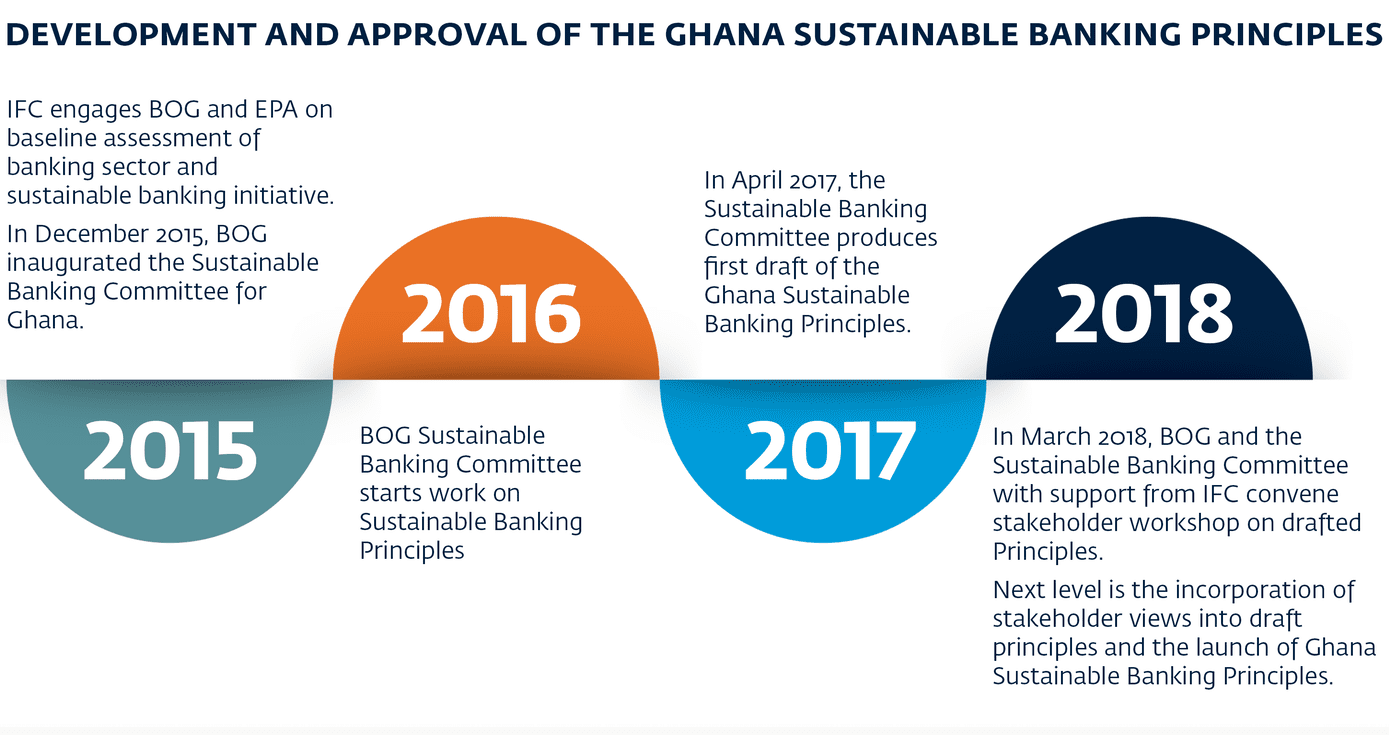

The genesis of the Ghanaian Sustainable Banking Principles can be traced to December 2015, when the Bank of Ghana inaugurated the Sustainable Banking Committee for Ghana with its mandate being the creation of local principles for the banking sector. The committee also comprised the Environmental Protection Agency (EPA), Ghana Association of Bankers (GAB) and six banks (Ecobank (chair), UT bank (then), Fidelity Bank, Société General, Barclays Bank and Stanbic bank).

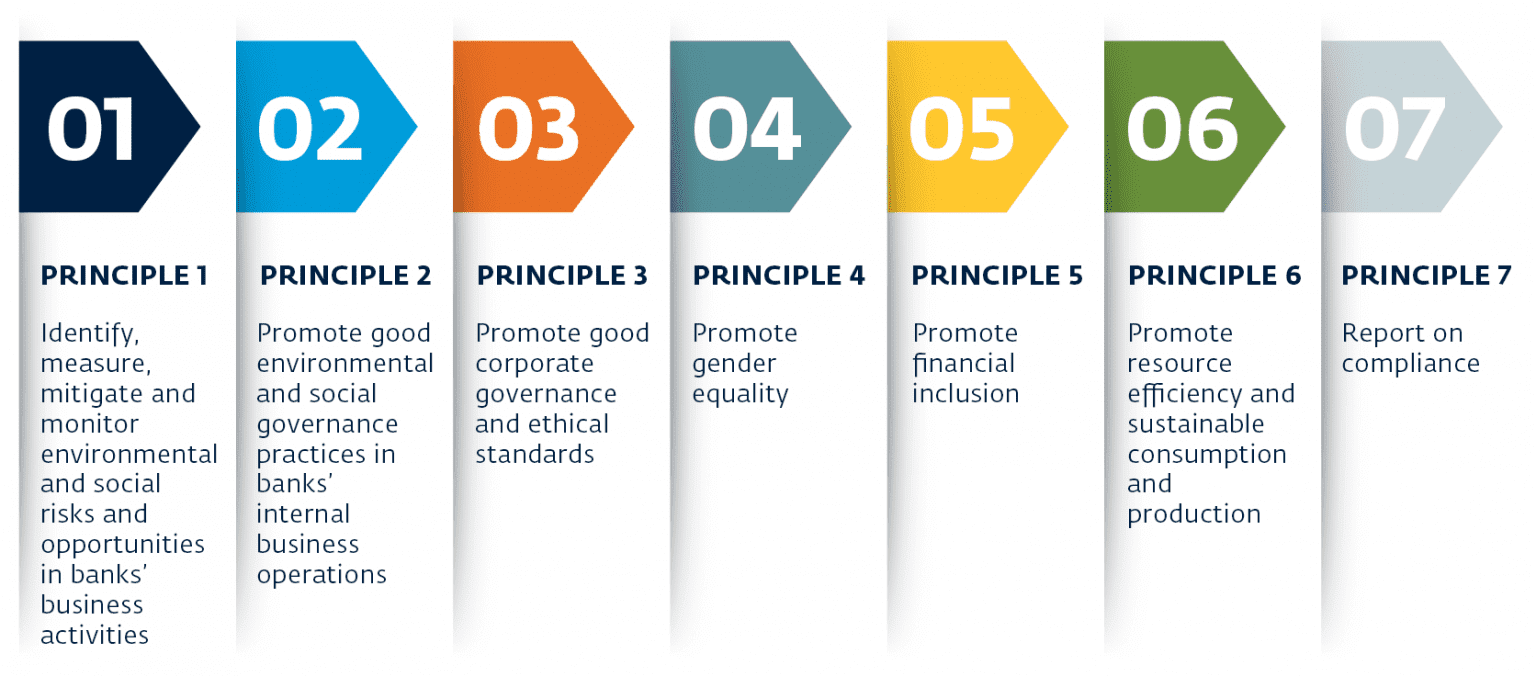

The framework is made up of seven principles that provide sustainability integration considerations for a bank’s business activities and operations. In addition, there are five sector guidelines that provide additional guidance to banks on lending to these high-risk sectors – Energy and Power, Construction and Real Estate, Agriculture and Forestry, Manufacturing, and Mining, Oil and Gas.

- Other Financial Sector Regulators

-

In Ghana, other financial sector regulators include the Ministry of Finance, Securities Exchange Commission, Ghana Stock Exchange and the National Insurance Commission.

Ministry of Finance

Ghana’s Finance Ministry is principally responsible for ensuring macroeconomic stability towards enhancing sustainable economic growth and development. Primarily, the functions of the Ministry include the formulation and implementation of sound fiscal and financial policies; effective mobilization and efficient allocation of resources; and the improvement of public financial management.

The Ministry of Finance, alongside the Ministry of Environment, Science and Technology, and the Environmental Protection Agencies, are key agencies in implementing Ghana’s Nationally Determined Contributions (NDCs) to Climate Change.

In April 2019, the Ministry signed a memorandum of understanding (MOU) with its partners including organised labour, the Ministry of Employment and Labour Relations, Trades Union Congress of Ghana and Ghana Employers Association. The MOU is geared towards achieving stronger collaboration and harmonious industrial relations. The Ministry is confident that this partnership will spearhead inclusive and sustainable growth towards transforming Ghana’s economy, expanding opportunities and creating jobs for all Ghanaians.

The Ministry of Finance also considers that to achieve the UN Agenda 2030 for Sustainable Development, Ghana needs to adopt growth-enhancing policies while containing risk and protecting the vulnerable. The Ministry will support relevant institutions and ministries such as the Ministry of Environment, Science and Technology to realise this goal. https://www.mofep.gov.gh/

Securities and Exchange Commission

The securities market in Ghana is regulated by the Securities and Exchange Commission (SEC). The SEC was established by the Securities Industry Act, 2016, (Act 929). The objective of the SEC is to regulate and promote the growth and development of an efficient, fair and transparent capital market in Ghana.

The SEC can encourage ESG disclosure for companies, including developing a framework for disclosure.

Ghana Stock Exchange

The Ghana Stock Exchange (GSE) is the main regulatory body in the stock exchange of Ghana. There are more than 40 listed companies on the GSE. Some of these companies include AngloGold Ashanti Depository shares, Access Bank Ghana, Agricultural Development Bank, AngloGold Ashanti Limited, CAL Bank, Ecobank Ghana Ltd and many others whose activities influence E&S risk considerations.

The GSE can key into the Sustainable Stock Exchanges initiative, a UN partnership initiative that promotes responsible investments and green bonds issuance guidelines.

National Insurance Commission

The National Insurance Commission (NIC) is responsible for regulating insurance business in Ghana. Apart from regulation, NIC also ensures effective administration and supervision of insurance businesses in Ghana. This includes licensing of entities, setting standards, approving rates of insurance premiums and commissions, providing the conduit for arbitration and complaints resolution, amongst others.

The NIC can key into the Principles on Sustainable Insurance (PSI), a United Nations framework that promotes ESG risk management for the industry.

National Pensions Regulatory Authority (NPRA)

The National Pensions Regulatory Authority (NPRA) is responsible for pension regulation through effective policy implementation aimed at securing sustainable incomes for retired Ghanaian workers. The Authority oversees the administration and management of registered pension schemes and trustees, as well as the Social Security and National Insurance Trust (SSNIT) management of the basic national social security scheme.

Key functions of the Authority include:

- Register occupational pension schemes, provident funds and personal pension schemes

- Establish standards, rules and guidelines for the management of pension funds under this Act

- Regulate and monitor the implementation of the Basic National Social Security Scheme

- Promote and encourage the development of the pension scheme industry in the country

- Advise government on the general welfare of pensioners

- Advise government on the overall policy on pensions in the country

Pension regulation is at the core of social cohesion amongst workers. This is why it is important that the NPRA develops sustainable pension policies that can lead to enhanced social benefits when workers retire. In this respect, the development of the contributory three-tier pension scheme, consequent to Act 766, will help ensure retirement income security.

Social Security and National Insurance Trust (SSNIT)

Under the National Pensions Act, 2008 Act 766 (amended in 2014), the Social Security and National Insurance Trust (SSNIT) is mandated to manage Ghana’s Basic National Security Scheme. This involves mandatory tier one contributions by all workers in Ghana. The Trust’s mission involves providing income security for workers in Ghana through excellent business practices.

In addition to being the largest non-financial institution in the country, the Trust is also the largest single institutional investor on the Ghana Stock Exchange. SSNIT has a vision of providing income security for workers in Ghana through excellent business practices. This falls within the social management and sustainability structure of employees’ welfare as the contributions managed by SSNIT on behalf of Ghanaian workers act as an economic and social safeguard when workers are on retirement. SSNIT could therefore use its investment in and provision of social protection schemes as a way of influencing financial inclusion among its members.

Ghana Insurers Association

Ghana Insurers Association is a membership body of all insurance and reinsurance companies that have been licensed to conduct insurance business within Ghana. Its vision is “to provide effective, efficient and disciplined leadership for sustainable growth in the insurance and economic development of Ghana”. The Association has over 50 members within the Life Insurance, General Insurance and Reinsurance sub sectors.

Within the insurance sector, the opportunity exists for GIA to help the financial sector achieve sustainability. In line with its sustainability principles if any, gender equality and financial inclusion can be enhanced. Insurance companies can also help mitigate banks’ E&S risks by insuring transactions in the financial sector that have potentially harmful E&S considerations.

- Sustainability Reporting

-

The reporting requirements for the Sustainable Banking Principles are captured in the seventh principle on reporting. It is expected that the Bank of Ghana will roll out monitoring and supervision of the principles in a phased approach.

It is good practice for the commercial banks to develop a sustainability reporting framework that can be published on the bank’s website. These reports should meet reporting requirements as indicated by the Global Reporting Initiative Financial Sector Supplement. Where necessary, independent third-party reviews and quality assurance of reports should be undertaken.

Globally, sustainability reporting performance has become an integral requirement for the issuing and renewing of licenses for companies to operate. Many organisations are moving towards producing integrated reports, instead of separate sustainability and financial reports, as this represents a more encompassing approach to managing environmental and social aspects as part of a business’s overall performance. This is a trend Ghanaian businesses and banks should embrace as part of their business operations. Producing integrated reports will make financial institutions more attractive to the international and development financial institutions and improve guidelines to monitor their environmental and social performance.

- Other Sustainability Initiatives in the Ghanaian Financial Sector

-

Various stakeholders and initiatives in Ghana promote the sustainable finance agenda in the country. These initiatives range from research to policy support and implementation and include important topics such as a green economy, sustainability reporting, green buildings, green bonds and many more.

- United Nations Partnership for Action on Green Economy (UN PAGE Initiative)

-

Following the United Nations (UN) Conference on Sustainable Development in Rio de Janeiro, the Partnership for Action on Green Economy (PAGE) was launched in 2013 as a joint initiative of the UN Environment, ILO, UNDP, UNIDO and UNITAR. PAGE exists primarily to support member countries who wish to undertake greener and more inclusive growth trajectories. PAGE believes that in developing any economic policies and practices, sustainability should be the overriding consideration. This will help advance the 2030 Agenda for Sustainable Development. PAGE offers support to countries that want to restructure their economic policies and practices around sustainability. The idea is to improve economic growth, create incomes and jobs, reduce poverty and inequality, and strengthen the ecological foundations of their economies.

In 2014, Ghana became a member of PAGE. As part of its activities, PAGE supports the country in identifying priority areas and provides guidance in key strategies and policy implementation. From 2014 to 2017, PAGE assisted in the implementation of the Ghana Shared Growth and Development Agenda (GSGDA II). In addition, it supported Ghana’s National Climate Change Policy and the UNDP-UNEP’s Green Economy Study and Assessment. More importantly, as the country made progress on sustainability, PAGE conducted a study which sought to analyse the green economy opportunities in Ghana, financial and private sector participation in green financing and investment, and the barriers to green financing. The overall goal was to support the Ghana government in reframing policy across sectors, and to build individual and institutional capacity to ensure sustainability and scaling up of green financing in Ghana. The study found that among many factors, the main drivers of green financing in Ghana are the environmental regulatory framework, commitment of relevant actors, globalization of standards in the financial sector, external stakeholder support, stakeholders’ gatekeeping role and the existing national sustainable development frameworks.

- United Nations Environment Programme – Finance Initiative (UNEP FI)

-

The United Nations Environment Programme – Finance Initiative (UNEP FI) is a collaboration between the United Nations Environment and the global financial sector. This partnership with the UN Environment has over 240 financial institutions including banks, investors and insurers working towards sustainable financing of environmental, social and governance operations.

In 2013, UNEP FI organised its first ever Introductory Environmental and Social Risk Analysis training program in Ghana. The workshop was organised with support from its member Ecobank and hosted by the Ghana Association of Bankers. Relevant stakeholders such as bank credit risk managers, loan portfolio officers and many others were trained on the need and importance of incorporating environmental and social considerations into their business operations. In 2018, UNEP FI, through colleagues at PAGE, also undertook a study to measure Ghana’s level of integration of sustainability into business decisions of the financial sector and its clients. In addition, the study created an opportunity to promote sustainability awareness within the business community.

- Global Reporting Initiative (GRI)

-

Global Reporting Initiative (GRI) is an international organization that engages businesses and governments on sustainability issues. Since 1997, GRI has spearheaded communication on Environmental and Social Risk including the impact of climate change, governance and social well-being and human rights. GRI seeks to influence decisions that result in environmental, social and economic benefits for all.

One of the ways in which they undertake to empower decision making is through the GRI Sustainability Reporting Standards. These Standards are the most widely accepted standards on sustainability reporting the world over. GRI Sustainability Reporting enhances accountability, helps manage risks and improves corporate governance in general. With the support from SECO (the Swiss State Secretariat for Economic Affairs), the sustainability reporting for SMEs to gain better access to global value chains was introduced in Ghana.

GRI core areas include:

- Creating standards and guidance to advance sustainable development

- Harmonizing the sustainability landscape

- Leading efficient and effective sustainability reporting

- Driving effective use of sustainability information to improve performance

- EDGE Building

-

The EDGE building certification tool was developed by the IFC to provide an easy and affordable system that can be leveraged by residential and commercial buildings to integrate green building design. EDGE comprises a web-based software application, universal standard and certification system. The EDGE program is supported by the Swiss donor agency – SECO.

- Climate Investment Fund (CIF)

-

The Climate Investment Fund is a funding vehicle geared towards bridging the financing and learning gap needed for climate change mitigation and adaptation. In Ghana, the CIF has approved investment plans in the Forest Investment Program (FIP) ($75million) and Scaling up Renewable Energy Program (SREP) ($40million). The World Bank and Africa Development Bank (AfDB) are the implementing multilateral development banks for the CIF projects

Ghanaian Environmental And Social Laws

Ghana’s economy is highly reliant on climate sensitive sectors such as agriculture, and thus, preservation of the environment, and awareness of social risks is important for a resilient economy. From a regulatory perspective, there are a myriad of regulations in Ghana addressing protection of the environment, and society. It is important for financial institutions to be aware of the pertinent legislation which is applicable to their clients’ businesses, as well as their own operations.

This section presents an overview of key environmental and social legislation, and the coordinating bodies pertinent for financial institutions.

Overview of E&S Regulations in Ghana

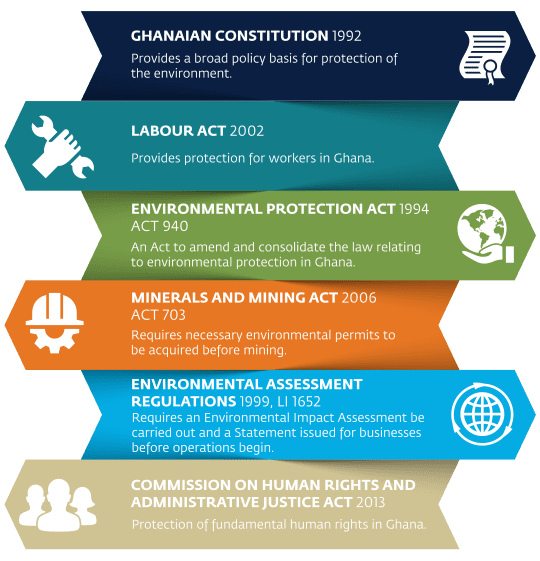

In 2001, the Ghana Environmental Assessment Capacity Development Programme (GEACaP) was launched with support from the Netherlands government. Primarily, the mandate of the program was to help all relevant institutions in achieving their respective obligations, and to promote sustainable economic development in Ghana. An important aspect of the programme was the development of Environmental Assessment Sector Specific Guidelines for eight main sectors of the economy. These included Health, Manufacturing, Transportation, Mining, Tourism, General Construction and Services, Agriculture and Energy. Consequently, representatives from these eight stakeholder sectors came together with the EPA to develop the sector specific obligations towards the environment. Similar environmentally enhancing activities in the past culminated in the establishment of the Environmental Protection Agency with powers to regulate the use of the environment and ensure the implementation of policies on the environment by the government. As a result, various interventions and policy instruments such as environmental impact assessments, Parliamentary Acts and legislation, environmental guidelines, environmental taxes such as reclamation bonds, and environmental permitting standards i.e. emission permits have been promulgated to address environmental problems. These laws, together with other legislations and regulations, primarily seek to operationalise the broad environmental policy directives in the 1992 Constitution of Ghana. It is therefore crucial that financial institutions are abreast with these rules and regulations while carrying out financial intermediation activities.

On the social regulations side, there exists many laws and regulations which cover the rights and safety of workers, the vulnerable in society and the social issues confronting communities. The fundamental human rights of every Ghanaian are enshrined in the 1992 Constitution. Other social and labour laws include the Labour Act, 2003, Act 651, the Children’s Act, 1998, Act 560 and the Commission on Human Rights and Administrative Act, 1993, Act 456. Ghana has also ratified other International Labour Organization (ILO) Conventions to guide the country in its labour and social issues. Some of these conventions guarantee workers the right and freedom to join or form worker unions (Convention No.87), the right to equal treatment (Conventions Nos. 100 and 111), the right to collective bargaining (Convention No. 98) as well as conventions to promote industrial harmony and welfare of workers. Among the institutions responsible for implementing these rules and regulations include the Commission on Human Rights and Administrative Justice (CHRAJ) and the National Labour Commission (NLC), the Ministry of Employment and Labour Relations, the National Tripartite Committee (NTC) etc.

- E&S Protections in the Ghanaian Constitution

-

Guidance on legislation:

The constitutional basis for E&S protections for Ghana which stipulates that the public lands in Ghana are vested in the president on behalf of the people of Ghana.

The 1992 Constitution provides a broad policy basis for the protection of the environment in Ghana. Article 257 stipulate that all public lands in Ghana are vested in the President on behalf of, and in trust for, the people of Ghana; with the President’s pledge to protect the Constitution. Specifically, the basis of Environmental Policy in Ghana is grounded in Article 36(9) of the 1992 Constitution. The Direct Principles of State Policy places a responsibility on every Ghanaian and the government to protect and safeguard the environment for posterity. It explicitly requires the government to take relevant steps aimed at the protection and defence of the national environment for future generations. The government is expected to do this in collaboration with appropriate agencies.

The Constitution also guarantees the fundamental human rights of every person found within Ghana. Chapter 5 of the Constitution, section 12(2) says that “Every person in Ghana, whatever their race, place of origin, political opinion, colour, religion, creed or gender shall be entitled to the fundamental human rights and freedoms of the individual contained in this chapter but subject to respect for the rights and freedoms of others and for the public interest”. These rights include right to life, right to a decent job, economic rights and women (gender) rights. It is worthy of note, that the entire Chapter 5 of the constitution, on human rights, is an entrenched clause, meaning it may only be amended by the people of Ghana through a referendum.

- Environmental Protection Agency (EPA) Act, 1994 (Act 490)

-

Guidance on legislation:

This establishes the Environmental Protection Agency (EPA) with the authority to act on environmental protection in Ghana. The EPA therefore monitors and ensures compliance of businesses with Ghanaian E&S laws. The EPA issues fines and penalties for businesses that are not in compliance.

Sequel to the 1992 national Constitution, the Environmental Protection Agency (EPA) Act, 1994 (Act 490) was passed. The Act subsequently established the Environmental Protection Agency (EPA). This Act, among other things, is “an Act to amend and consolidate the law relating to environmental protection, pesticides control and regulation and for related purposes.” It provides for the powers as well as the governing body of the Environmental Protection Agency. The Act among other things also establishes the Hazardous Chemicals Committee and empowers the Board to create such departments and divisions as and when necessary. It also repealed the Environmental Protection Council Decree, 1976. The EPA is the main body vested with the authority to administer environmental laws in Ghana. It is therefore important that financial institutions, in granting loans to business entities whose activities affect the environment, do so after having satisfied themselves with the environmental assessment reports from their clients.

- Environmental Assessment Regulations, 1999, LI 1652

-

Guidance on legislation:

Businesses with environmental activities are required to register with the EPA and duly receive permitting to operate.

Financial institutions must ensure that their clients have the proper permitting to operate as failure to do so will result in fines and other penalties. Financial institutions may also require the permitting for their banking operations.

The Environmental Assessment Regulations (EAR) were made in 1999 pursuant to the EPA Act, 1994 (Act 490). Primarily, the EAR (amended in 2002) requires that before the commencement of any activity which relates to the environment, such an activity or undertaking be registered by the EPA and an environment permit issued in respect of the undertaking. As such, activities such as mining, construction, logging, oil marketing etc which have the potential of adversely affecting the environment must first go through an Environmental Impact Assessment, leading to the production of an Environmental Impact Statement (EIS). Thus, the objective is to guarantee that economic activities are carried out in a sustainable and environmentally and socially conducive manner. These regulations are broad and require different kinds of stakeholders to shoulder different responsibilities. In the case of financial institutions for example, it is inherent on banks to confirm environmental impact assessment reports (statements) before approving credit requests for activities that potentially have an adverse impact on the environment. Banks themselves must also get permits for their branches. According to the EPA, the EAR, LI 1652, gives a comprehensive legal cover to the Ghana Environmental Impact Assessment procedures.

- Minerals and Mining Act, 2006, (Act 703)

-

Guidance on Legislation:

Businesses undertaking minerals and mining operations must receive a mining license before commencement of activities from the Forestry Commission and EPA.

Financial institutions must ensure that their clients can present this license

The Minerals and Mining Act requires that, among other things, a holder of a mining license, before commencing mining activities, must obtain the necessary environmental permits. The Act specifically states that;

“(1) Before undertaking an activity or operation under a mineral right, the holder of the mineral right shall obtain the necessary approvals and permits required from the Forestry Commission and the Environmental Protection Agency for the protection of natural resources, public health and the environment.

(2) Without limiting subsection (1), a holder of a mineral right shall comply with the applicable Regulations made under this Act and any other enactment for the protection of the environment in so far as relates to exploitation of minerals.”

- Labour Act, 2003, Act 651

-

Summary of legislation:

The labour act prohibits discrimination based on sex, ethnicity, race, colour, religion etc and provides protection for workers in Ghana.

Financial Institutions should ensure that both the human resource (HR) policies and terms of employment of the FI and the bank are in line with labour laws.

The Labour Act, 2003, repealed the Industrial Relations Act, 1960, Act 299 which hitherto governed labour relations in Ghana. Under this act, the Labour Department under the then Ministry of Labour Affairs was responsible for dealing with labour disputes. Many have described Act 651 as a consensus law because all the stakeholders, namely Organised Labour, Government and Ghana Employers Association had to lose in some respects and win in other aspects of the negotiation to arrive at Labour Act, 2003, Act 651.

- Commission on Human Rights and Administrative Justice Act, 1993, Act 456

-

Guidance on Legislation:

The established implementing body is tasked with investigating human rights complaints.

Financial institutions should ensure that they and their clients have grievance mechanisms in place for workers to raise reasonable workplace complaints.

The Commission on Human Rights and Administrative Justice (CHRAJ) Act, is an act that empowers the implementing body, CHRAJ, with the mandate to look into “complaints of violations of fundamental human rights and freedoms, injustice and corruption; abuse of power and unfair treatment of persons by public officers in the exercise of their duties, with power to seek remedy in respect of such acts or emissions and to provide for other related purposes”. Section 7 (1) (a) (c) and (g) of the CHRAJ Act specifically mandates the body to ensure the fundamental human rights and freedoms of persons in Ghana are protected irrespective of colour, tribe, nationality etc.

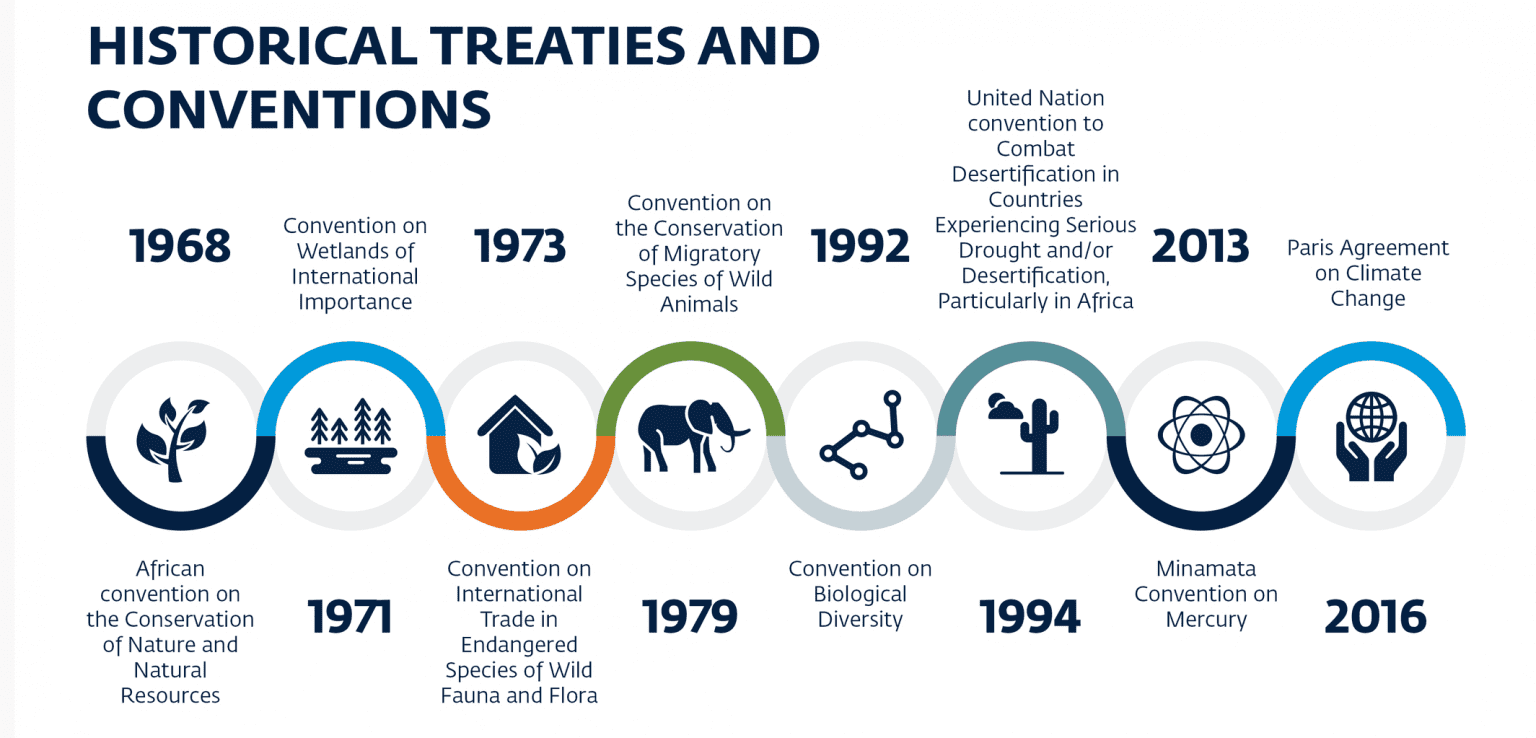

International Environmental and Social Conventions Signed and Ratified by Ghana

Ghana has remained a signatory to many international conventions and treaties that address Climate Change, the Environment and its Sustainability. In 2005 a body was set up at the Ministry of Environment, Science and Technology (MEST) called the Ghana Environmental Convention Co-ordinating Authority (GECCA) to co-ordinate the ratification (in some cases) and implementation of these international conventions and treaties on the environment. Some of these Conventions and Treaties include Cartagena Protocol on Biosafety, Stockholm Convention on Persistent Organic Pollutants, Kyoto Protocol to the United Nations Conventions on Climate Change, Paris Agreement on Climate Change etc

There are many other laws which regulate environmental use in Ghana. Some of these laws and regulations include the Hazardous and Electronic Waste and Management Act, 2016 (Act 917) which prohibits the importation, exportation, transportation, selling, purchasing or dealing in or depositing of hazardous waste or any other waste within Ghana or her territorial waters and the Petroleum Exploration and Production Act, 2016, Act 919, an act which provides the enabling requirement for participation in Ghana’s petroleum industry by the private sector.

International Labour Organizations Conventions ratified by Ghana

In 1957, Ghana became a member of the ILO and has since ratified many of the Organization’s Conventions aimed at socially and economically enhancing Ghanaian labour force. Some of the ratified Conventions include Equal Remuneration Convention (#100), Discrimination (Employment and Occupation) Convention (#111), Freedom of Association and Protection of the Rights to Organise Convention (#87), Right to Organise and Collective Bargaining Convention (#98), Forced Labour Convention (#29), Abolition of Forced Labour Convention (#105), Working Environment (Air Pollution, Noise and Vibration) Convention (#148), Labour Relations (Public Service) Convention(#151) etc. In total, Ghana has ratified 51 Conventions, of which 37 are in full force, 10 of them have been denounced and 4 abrogated.

Ghanaian E&S Regulatory Agencies

Regulatory institutions are the conduit through which environmental and social legislation is implemented in Ghana. Any project or activity which has the potential of adversely affecting the environment will require regulation.

Financial institutions should be aware of the implementing regulatory agencies for E&S legislations.

- Ministry of Environment, Science, Technology and Innovation (MESTI)

-

The mandate of the Ministry is to promote sustainable development through relevant and thought-provoking research and development in its four main areas, sound environmental governance, technology, science and innovation. Created in 1993 and having undergone name changes along the way, the Ministry’s main functions in relation to the environment among others include the following;

- To provide leadership and guidance in its main area through the formulation and implementation of sound policies within the broad sector of the economy.

- In charge of establishing standards and the regulatory framework for the Environment, Science and Technology within which sustainable development can be achieved.

- Initiates and co-ordinates research aimed at improving the laws, rules, policies and regulations that govern the environment.

- Ensures effective environmental management and governance

- Determines the requirements for any programme on the environment, science, technology and human settlement.This it does in consultation with the National Development Planning Commission (NDPC).

There are many agencies under the Ministry which execute some of these functions. These agencies include;

- Council for Scientific and Industrial Research

- Atomic Energy Commission of Ghana

- Environmental Protection Agency

- Land Use and Spatial Planning Authority

- National Biosafety Authority

- Environmental Protection Agency

-

Established in 1994, the Environmental Protection Agency (EPA), is the main body responsible for regulating or administering environmental laws in Ghana and falls under the Ministry of Environment, Science, Technology and Innovation (MESTI). The Agency was established consequent to the Environmental Protection Agency Act, 1994 (Act 490). In 2001, the Ghana Environmental Assessment Programme (GEcAP) helped the EPA streamline the various sector specific environmental requirements and policies. Among the many functions as spelt out in the Act, its main functions include the following;

- Advises the (Sector) Minister on the formulation of policies and recommendations for the protection of the environment;

- Acts as a co-ordinating body for technical or practical entities whose activities affect the environment and serves as a channel of communication between those bodies and the Ministry;

- Issues environmental permits and pollution abatement notices for activities which are potentially dangerous to the quality of the environment or parts of it;

- Issues directives, procedures or warnings to any other person or body for controlling the volume, intensity and quality of noise in the environment;

- Ensures compliance with the laid down environmental impact assessment procedures in the planning and execution of development projects and/or existing projects.

- Minerals Commission of Ghana

-

These include but not limited to the Lands Commission, Minerals Commission Forestry Commission etc. The Minerals Commission is one of the agencies of the Ministry of Lands and Natural Resources. Established under the 1992 Constitution (Article 269) and the Minerals Commission Act 1993, Act 450, it is the main regulatory body in the minerals and mining sector. Pursuant to the above legislation, the Minerals Commission is responsible for “the regulation and management of the utilization of policies relating to mining.” In addition, the Minerals Commission also makes sure that Ghana’s Mining and Mineral Laws and Regulations are also complied with. This is done mainly through effective monitoring and evaluation of mining activities especially on the environment and natural resources. In monitoring mining companies, the Minerals Commission liaises with other State agencies such as the EPA, Bank of Ghana and Geological Survey Department to help attain adherence of the requirements of a competitive fiscal regime as well as the mineral rights granted to these mining companies.

- Petroleum Commission of Ghana

-

In regulating activities in Ghana’s upstream petroleum sector, the Petroleum Commission is the main body responsible for this activity. Its counterpart, the National Petroleum Authority regulates petroleum activities in the downstream sector. The Petroleum Commission was established by an act of Parliament, Act 821, in 2011. Together with other agencies such as the Energy Commission, Ghana National Petroleum Commission (GNPC), Ghana National Gas Company (Ghana Gas) and Environmental Protection Agency (EPA), the Petroleum Commission regulates and manages the utilization of the country’s oil and gas resources. It also co-ordinates any other activity to do with sustainability in the upstream sector.

- Energy Commission

-

Like the Petroleum and Minerals Commissions, the Energy Commission is also involved in the regulation of aspects of Ghana’s natural resources such as natural gas. The Commission is the technical regulator of the country’s renewable energy environment as well as its electricity landscape. Set up by the Energy Commission Act, 1997, Act 541, the Commission’s mandate also includes management, development and utilization of Ghana’s energy resources “in a reliable, efficient and secure manner in order to promote the social and economic well-being of the people of Ghana, enhance environmental quality and public safety.”

- Water Resources Commission

-

In 1996, the Water Resources Commission was established by a Parliamentary Act (522). Its mandate includes regulating and managing Ghana’s water resources as well as streamlining government policies in the water resources industry. In the same way that all land is vested in the President on behalf of the people, it is the same with country’s water resources. Ownership and management of Ghana’s water resources are vested in the President on behalf of the Ghanaian people. The Commission comprises of 15 members, drawn from various sectors of the economy.

- National Labour Commission

-

The National Labour Commission (NLC) was established as required by the Labour Act, 2003. Section 35 of the Labour Act stipulates that an NLC be established to among other things, mediate in settling industrial disputes via negotiations and other dispute resolution methods such as mediation and arbitration. The NLC also works towards promoting a sustainable and harmonious working environment through effective dispute resolution mechanisms and settlements. Under the Ghana Shared Growth and development Agenda, the NLC seeks to;

- Promote a harmonious labour relations environment

- Compliance with the laws regulating the employment relationship

- Adherence to procedures for addressing industrial disputes/ disagreements

- Commission on Human Rights and Administrative Justice

-

The Commission on Human Rights and Administrative Justice (CHRAJ) came into being under the 1992 Constitution. Broadly, the Commission is involved in three main areas; human rights, administrative justice and anti-corruption fight. It is the duty of the institution to promote and protect the fundamental human rights and freedoms of every citizen. These rights include civil, social, economic, political etc. The human rights function of the Commission is categorized into; promotion and prevention as well as protection and enforcement.

- National Tripartite Commission (NTC)

-

Under the 2003 Labour Act, one of the requirements of the act was the establishment of a National Tripartite Committee which will compose of the Government of Ghana, Organised Labour, and Ghana Employers Association. The Minister of Employment and Labour Relations is the chairman of the Committee. Primarily, the NTC is the body mandated to determine the National Daily Minimum Wage. It also gives advice to the ministry on labour and employment issues. This could include economic and social issues.

Sustainability In The Nigerian Financial Sector

Nigeria’s banking sector plays a significant role in the country’s growth and is critical to the overall development of the economy. Sustainability was initially approached by the sector from a primarily corporate social responsibility (CSR) angle, with financial institutions supporting charitable initiatives and community engagement activities. However, following numerous significant global events such as the 2016 Paris Climate accord, Annual UN Climate Change Summits, and many international financial institutions resorting to green financing, sustainable investing has finally elbowed its way into mainstream financial intermediation.

With these new economic realities and growing complexities of the operating environment, the Nigerian banking sector has over the years begun to pay closer attention to environmental and social sustainability of the companies it finances. In line with global trends, Nigerian banks have developed a sector-wide framework on sustainable banking, namely the Nigerian Sustainable Banking Principles (NSBP).

- Overview of The Nigerian Banking Sector

-

Nigeria is the largest financial market in Africa. As of November 2018, 21 commercial banks were licenced by the Central Bank of Nigeria (CBN). Nigeria has a relatively well-developed banking sector by regional standards, with regionally high level of banking penetration (44.2% vs. regional average of 17.8% for West Africa) and robust use of advanced financial instruments in the local economy. The country is also well connected to international financial markets and following the 2016-17 oil crisis, the country has seen an increasing influx of foreign capital over the past 12-18 months – capital importation in Nigeria jumped to US$6.3 bln in Q1-18 (594% yoy growth) vs. $12.3 bln for full year 2017 and $5.1 bln in 2016). However, the country is weighed down by high lending rates, which limits access to credit for smaller firms, particularly in the non-oil economy.

Nigeria’s banking sector has recovered strongly from a combination of weak governance and the effects of the global recession in 2009. Though contending with multiple challenges including macro-economic uncertainties, cyber risk, increased competition from alternative banking channels, increased regulations, and a restive customer base demanding effective and flexible banking services, the outlook for the industry is positive.

- The Nigerian Sustainable Banking Principles

-

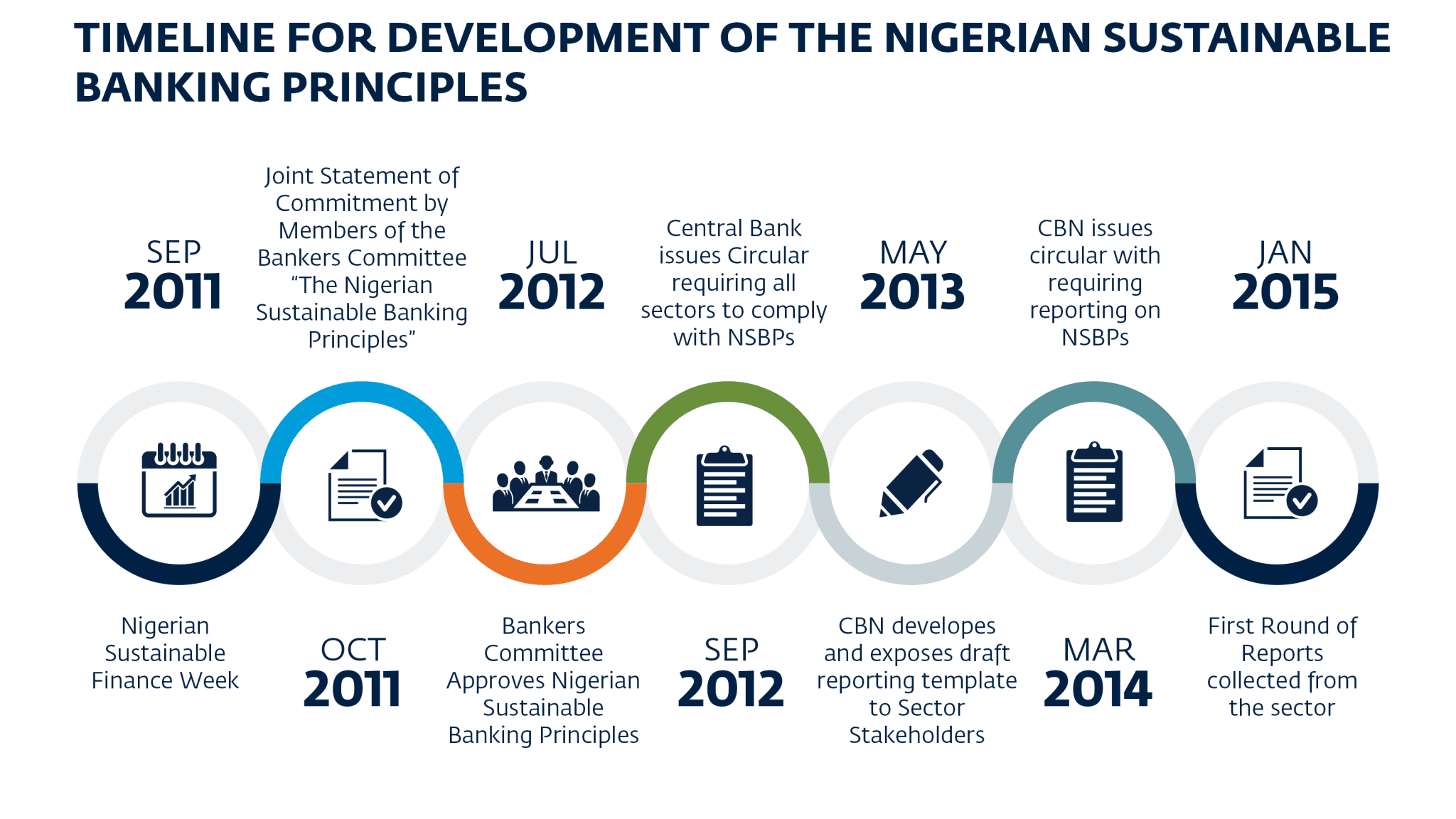

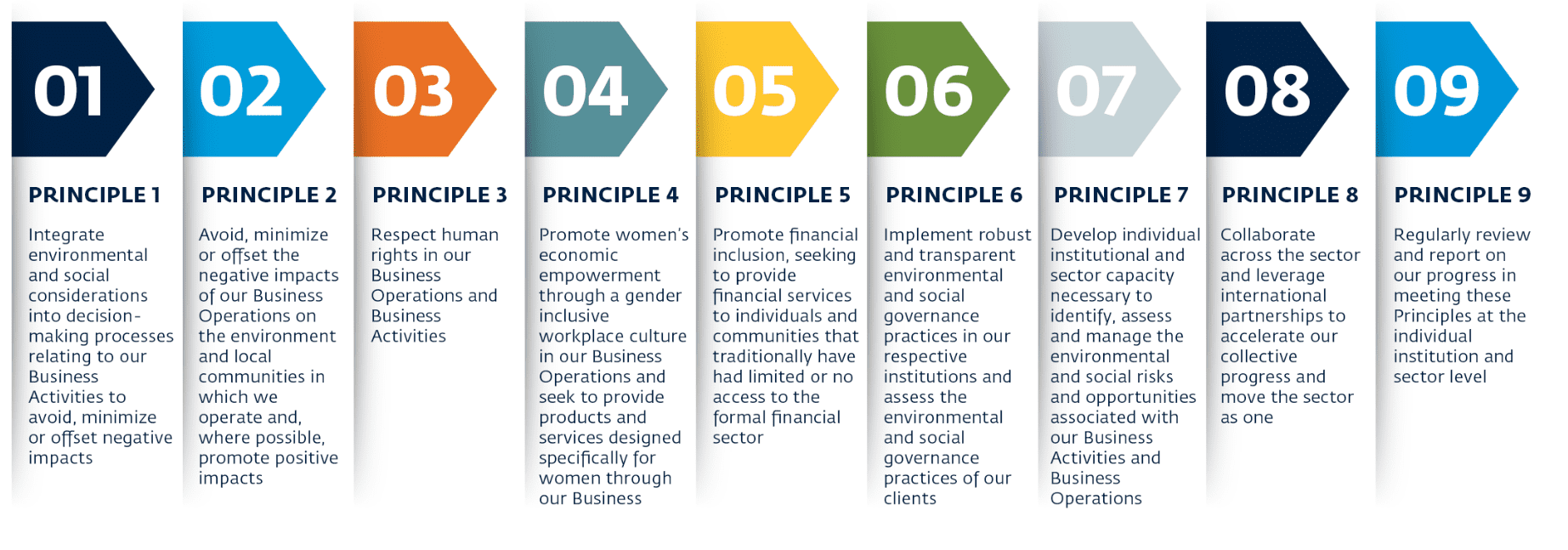

In 2011, the Nigerian banking sector commenced discussions on adopting a sustainable banking framework, which culminated in the establishment and adoption of the Nigerian Sustainable Banking Principles (NSBP), a set of nine guiding principles and three sector guidelines tailored to the Nigerian operating environment, and presenting a best practice framework for integrating environmental and social considerations into business activities and operations of financial institutions.

Background on the Nigerian Sustainable Banking Principles

The start of conversations on sustainable banking in Nigeria began in 2011 with the convening of the industry at a Sustainable Finance week, organized by the United Nation Environment Program Finance Initiative (UNEP FI). They apply to all lending instruments, project and structured commodity finance, equity and debt capital market activities, retail banking and advisory services.

The first major milestone was the Joint Commitment Statement, which was issued by the Bankers’ Committee in October 2011 stating the sector’s commitment to sustainability and the development and implementation of the principles. The statement was signed by all commercial bank chief executive officers (CEOs), the then Central Bank of Nigeria (CBN) Governor and CEOs of major discount houses.

The Strategic Sustainability Working Group (SSWG) was established under the Bankers’ Sub-Committee on Economic Development and Sustainability to coordinate the process. The SSWG consists of representatives from six banks – Access Bank, Zenith Bank, Standard Chartered, Diamond Bank, Citibank and GT Bank; representatives from the IFC, FMO, CBN, National Deposit Insurance Corporation (NDIC); and an independent adviser.

In addition to the development of an overarching set of Sustainable Banking Principles to be applied to all sectors, the SSWG was also tasked with developing specific guidelines for three strategic sectors:

- Agriculture – to ensure integration of sustainability aspects in the Nigeria Incentive Based Risk Sharing System for Agricultural Lending (NIRSAL) framework. NIRSAL is a joint response by the CBN, the Banker’s Committee and the Federal Ministry of Agriculture and Rural Development to address the challenge of low levels of lending to and investment in the agricultural sector

- Power and Renewable Energy – with the intention of encouraging private sector participation in the financing of renewable energy

- Oil & Gas – in recognition of the significant environmental and social impacts associated with the sector

The Nigerian Sustainability Banking Principles, in conjunction with the CBN circular, provides the framework for banks to include the consideration of environmental and social risks in their lending and investment activities and to implement this through their operational and enterprise risk management and other governance frameworks. Furthermore, the CBN intends to establish reporting requirements to enable the regulator to track progress of implementation of and adherence to the Principles.

CBN Circular on “Implementation of Sustainable Banking Principles by Banks, Discount Houses and Development Finance Institutions in Nigeria”

Timeline on Nigerian Sustainable Banking Principles development

Following the adoption of the Principles, the Central Bank of Nigeria (CBN) developed a draft reporting template for banks to report on their compliance with the principles. The template presented a way of ensuring uniformity in reporting across the sector. The template was disseminated to the sector in May 2013 for comments and feedback. Following this, feedback was incorporated and a finalized reporting template was issued to the sector in March 2014.

The reporting requirements are grouped in two phases – Phase 1 delivers the Year 1 Milestones (also called the ‘one-off reports’). Phase 2 reporting delivers Year 2 and onward reporting for the banks.

In summary, Phase 1 – ‘Year 1 Milestones’ submissions include:

- A Sustainable Banking Commitment statement articulating a five-year timeline and procedures for integrating the Principles into the Bank’s Enterprise management framework

- An engagement strategy for the bank’s senior management and board of directors, and a capacity building program for relevant stakeholders

- A specialized unit responsible for implementing and reporting on the Principles

- A board approved environmental and social management policy and procedures for banks business activities and operations highlighting details of scope and processes

n summary, Phase 2 – ‘Year 2 and onward’ submissions include:

- A detailed report on the implemented environmental and social policies and procedures

- Delivery against specified targets and milestones

- List of trained business units against the principles

In addition to these reports, the CBN requires the banks to submit:

- Regular reports to management and relevant board committees on its sustainable banking activities

- Standalone annual sustainability/corporate social responsibility report or inclusion of sustainability section in integrated annual report

Phase 1 reporting was collected between March 2014 and January 2015. Phase 2 reporting is expected on an annual basis. Reporting is expected to be submitted through the CBN’s online Electronic and Financial Analysis and Surveillance System (eFASS).

Supervision of the principles are the responsibility of the CBN’s Banking Supervision Department.

Reporting on the Nigerian Sustainable Banking Principles

Joint Statement of Commitment by Members of the Bankers Committee

“The Nigerian Sustainable Banking Principles”

As leaders in the Nigerian financial sector, we are uniquely positioned to further economic growth and development in Nigeria through our regulatory, lending and investment activities across a diversity of segments and sectors of the Nigerian economy. The context in which we make business decisions is, however, characterized by complex and growing challenges relating to population growth, urban migration, poverty, destruction of biodiversity and ecosystems, pressure on food sources, prices and security, lack of energy and infrastructure and potential climate change legislation from our trade partners, amongst others.

Increasingly, it has been demonstrated that the development imperative in Nigeria should not only be economically viable, but socially relevant and environmentally responsible. We recognize that we have a role and responsibility to deliver positive development impacts to society whilst protecting the communities and environments in which we operate – for today’s generation as well as for future generations. We believe that such an approach, one of sustainable banking, is consistent with our individual and collective business objectives, and can stimulate further economic growth and opportunity as well as enhance innovation and competitiveness.

Given the above considerations, we are prepared to take steps to ensure that our business decision-making activities take these considerations into account and are, where applicable, consistent with applicable international standards and practices, but with due regard for the Nigerian context and distinct development needs.

Consequently, we hereby state our commitment to developing and launching a voluntary set of Nigerian sustainable banking principles which will include:

- An overarching set of guidelines relating to our: (a) direct impacts on communities and the environment as a result of our own business operations; and

- ndirect impacts on communities and the environment as a result of our lending and investment activities;

- A set of sector-specific guidelines, including as a first priority: (a) oil and gas; (b) power (with a focus on renewable energy); and (c) agriculture and related water resource issues;

- A commitment to raising awareness and developing meaningful and lasting local capacity to manage emerging environmental and social risks and opportunities within our internal operations, as well as to relevant financial sector government agencies, learning institutions and service providers.

In developing these sustainable banking principles, we recognize the need for a process which involves the engagement of relevant stakeholders and industry experts. We also recognize the need for an approach which provides for appropriate levels of transparency, accountability and self-assessment through regular reporting to our stakeholders. We will seek to work with the Central Bank of Nigeria, other relevant government agencies and development finance institutions to create the enabling environment as well as the incentives and enforcement mechanisms required for successful adoption and uptake of the sustainable banking principles.

We acknowledge that we can better support environmentally and socially responsible economic development in Nigeria by joining forces rather than standing alone. We hereby sign this Joint Commitment Statement with the aim of developing a set of sustainable banking principles for the Nigerian banking sector, to drive long-term sustainable growth whilst focusing on development priorities, safeguarding the environment and our people, and delivering measurable benefits to society and the real economy.

The Principles in detail

- Sector Specific Guidelines

-

The Nigerian Sustainable Banking Principles include sector specific guidelines for engaging in three sectors considered priorities due to their high-risk natures and the high level of exposure by financial institutions to these sectors in Nigeria.

- 1. Agriculture Sector Guideline

-

Scope and Applicability

- Financial products and services in the agriculture value chain

- Nigeria Incentive Based Risk Sharing System (NIRSAL) lending

This Guideline applies to all lending instruments, project and structured commodity finance, equity and debt capital market activities, retail banking and advisory services provided to new and existing clients in the agricultural sector. The extent to which the Principles apply will depend on the level and nature of agriculture sector business activities financed by a Bank. Retroactive application of environmental and social requirements under this Guideline is not required for existing clients. The Guideline and its environmental and social requirements will, however, apply to any additional new facilities or services for existing clients.

- 2. Power Sector Guideline

-

Scope and Applicability

- Power generation sources and associated facilities (i.e. oil, gas and hydropower), except nuclear

- Electricity distribution and transmission infrastructure (e.g. upgrades or extensions)

- Alternative sources of power generation and associated facilities (e.g. solar, clean coal, wind, biomass, etc.)

The Guideline applies to all corporate lending, project and structured finance, equity and debt capital market activities, and advisory services provided to new and existing clients in the power sector. The extent to which the Principles apply will depend on the level and nature of power sector business activities financed by banks. Retroactive application of environmental and social requirements under this Guideline is not required for existing clients. The Guideline and its environmental and social requirements will, however, apply to any additional new facilities or services for existing clients.

- 3. Oil and Gas Sector

-

Scope and Applicability

- Upstream

- Exploration activities – aerial and seismic operations

- Appraisal drilling

- Development and production (including processing and initial storage)

- Transportation

- Decommissioning and rehabilitation

- Downstream

- Product refining

- Transportation and distribution activities – via pipelines, roads (trucks) and sea vessels

- Marketing – including product importation and storage

- Servicing

- Provision of technical support services for the upstream and downstream segments in the areas of drilling, well completion, well simulation, logistics, equipment supplies, etc.

The Guideline applies to all corporate lending, project and structured finance (including structured commodity finance), equity and debt capital market activities, and advisory services provided to new and existing clients in the oil and gas sector. The extent to which the Principles apply will depend on the level and nature of oil and gas sector business activities financed by a bank. Retroactive application of environmental and social requirements under this Guideline is not required for existing clients, however the Guideline and its environmental and social requirements will apply to any additional new facilities or services for existing clients.

- Upstream

- Related Documents

- Environmental and Social Policies of the Nigerian Financial Intermediaries

-

The Nigerian Sustainability Banking Principles (NSBPs) require banks to commit to adopting and implementing international environmental and social standards in their Environmental and Social Policy Statements, such as the Equator Principles, IFC Performance Standards and UN Global Compact. The environmental and social policy of banks forms a part of their Environmental and Social Management System (ESMS). An ESMS builds on the policy, with procedures, tools and staff capacity needed to effectively identify and manage banks’ environmental and social risk.

The NSBPs also require banks to include commitments in their Environmental and Social Policy or develop specific standalone policies on the following environmental and social aspects:

- Human Rights, consistent with the United Nations Universal Declaration on Human Rights, the Nigerian Constitution and local laws

- Gender equality and women’s economic empowerment issues

- Financial inclusion, financial literacy and the promotion of consumer protection

- Environmental and social procurement requirements for suppliers, contractors, and other third-party service providers

Banks are also required to develop a sector-specific environmental and social approach and policy for their power, agriculture, oil & gas business activities, due to the high-risk nature of these sectors. Guidance on managing the environmental and social risks associated with these sectors can be found in the NSBPs’ sector specific guidelines.

IFC Performance Standard 1 provides guidance on overarching policy development defining environmental and social objectives and principles. In addition, financial institutions are required to incorporate the Equator Principles into credit and risk management policies.

Related Documents

First for Sustainability: Guidance on developing and implementing environmental and social policy

IFC Performance Standard 1: Assessment and Management of Environmental Risks and Impacts

- Sustainability Reports for Nigerian Financial Intermediaries

-

Principle 9 of the Nigerian Banking Sustainability Principles (NSBP) requires banks to “regularly review and report on – progress in meeting these Principles at the individual institution – level.”

The NSBP Guidance Note requires that reporting to external stakeholders on progress against the Principles and banks’ sustainable banking commitments, policies and procedures be undertaken annually.

Banks should aim to produce sustainability reports on an annual basis as a standalone report, or preferably as an integral part of their annual report to shareholders. The report should meet reporting requirements specified in the Global Reporting Initiative Financial Sector Supplement. Where appropriate, independent third-party reviews and assurance of reports should be undertaken.

Internationally, reporting on sustainability performance is becoming an essential part of a company’s license to operate. Many larger companies are moving towards producing integrated reports, rather than standalone sustainability reports, as they represent a more holistic approach to managing environmental and social aspects as part of a business’s overall performance. In Nigeria, there is a trend towards sustainability and integrated reporting amongst large corporates.

Benefits for banks on producing sustainability reports include becoming more attractive to development and international financial institutions, increased accountability from stakeholders, and improved processes and systems to track and manage environmental and social performance.

- Related Documents

-

First for Sustainability Portal: Sustainability Reporting

Nigerian Sustainable Banking Principles Reporting Template

Getting More Value Out of Sustainability Reporting

Nigerian Sustainable Banking Principles

The Benefits of Sustainability Reporting

Need to Get Up to Speed on Integrated Reporting?

What does an Integrated Report look like?

Preparing an Integrated Report: A Starters Guide

- Key Financial Services Regulators/Actors

-

The primary regulator of the banking sector is the Central Bank of Nigeria (CBN), reporting to the Federal Ministry of Finance. The CBN Act of 2007 of the Federal Republic of Nigeria charges the bank with the overall control and administration of the monetary and financial sector policies of the Federal Government with the aim of:

- Ensuring monetary and price stability

- Issuing legal tender currency in Nigeria

- Maintaining external reserves to safeguard the international value of the legal tender currency

- Promoting a sound financial system in Nigeria

- Acting as banker and providing economic and financial advice to the Federal Government

To promote a sound financial system, the bank is charged with administering the Banks and Other Financial Institutions (BOFI) Act (1991) as amended, through its supervision and policy regulation activities, as well as the promotion of an efficient payment system. In addition to its core functions, CBN has over the years performed major developmental functions focused on all the key sectors of the Nigerian economy – financial, agricultural and industrial. Overall, these mandates are carried out by the bank through its various departments.

The Banker’s Committee also plays an important coordination role for the sector. The Committee is made up of the chief executive officers of all licensed banks in Nigeria. Its role is to examine and make recommendations on major issues affecting the banking industry; facilitate communication between the banks, sector regulators and the Federal Government; facilitate the development of manpower for the sector; review banking tariffs; make proposals on matters of banking, finance and the national economy; interpret banking policies and laws; resolve misunderstandings and conflicts; and prepare codes of conduct.

- Other Financial Sector Regulators

-

In Nigeria, other financial service sector regulators include the National Deposit Insurance Corporation (NDIC), Securities and Exchange Commission (SEC), Nigerian Pension Commission (PENCOM) and the Nigerian Insurance Commission (NAICOM), amongst others. The Financial Services Regulation Coordinating Committee (FSRCC) is a statutory committee, set up as an inter-agency body to address issues of common interest and concern to 10 regulatory and supervisory authorities in the financial services industry, including the CBN and agencies listed below.